Mortgage Application Documents Checklist (2026 Edition)

Mortgage Application Documents Checklist: 2026 Edition for DMV Homebuyers

By Ken Byrne, NMLS #187129 · ALCOVA Mortgage LLC, NMLS #40508 · Updated May 2026

Quick Answer: To apply for a mortgage in 2026, you'll need: government-issued ID, two years of W-2s and tax returns, recent pay stubs covering 30 days, two months of bank and asset statements, residence history, and explanations for any large deposits or credit items. Self-employed borrowers need additional business documentation. Submit clean PDFs — not phone photos — and respond to lender requests within 24 hours to keep your loan on schedule.

Key Takeaways

- Two-year rule: Lenders verify two full years of income, employment, and (for self-employed) tax returns — gaps require written explanation.

- 60-day asset window: All bank, brokerage, and retirement statements must cover the most recent 60 days — every page, every account.

- Source every deposit: Any non-payroll deposit over roughly 50% of your monthly gross income needs documented sourcing.

- Gift funds require a paper trail: Signed gift letter, donor's bank statement, and proof of transfer — no exceptions on conforming or government loans.

- Self-employed = more docs: Two years of personal and business returns, year-to-date P&L, and business bank statements.

- Speed wins: Pre-approvals stall most often from slow document delivery, not credit problems — return requests within 24 hours.

Table of Contents

- Why Documentation Drives Your Mortgage Timeline

- The Master Document Checklist at a Glance

- Personal Identification & Residency

- Income Documents for W-2 Employees

- Income Documents for Self-Employed Borrowers

- Asset & Bank Statement Documentation

- Down Payment Sourcing & Gift Funds

- Debt & Credit Documentation

- Property Documents (After You're Under Contract)

- Special Documents by Loan Type (VA, FHA, USDA, Jumbo)

- Common Documentation Mistakes That Delay Closings

- When Documents Are Due: The Loan Timeline

- Putting It All Together

- Frequently Asked Questions

- Glossary of Mortgage Document Terms

If you've ever heard a homebuyer say their mortgage "fell apart at the last minute," the actual cause was almost certainly a document problem — a missing bank page, an unexplained deposit, or a tax return that didn't quite match the pay stubs. Lenders don't reject good borrowers. They reject incomplete files.

The good news: every document a lender will ever ask for is predictable. There are no surprises if you know what's coming. This 2026 checklist walks through exactly what underwriters at ALCOVA Mortgage — and every conforming, FHA, and VA lender in the DMV — require, why they require it, and the quiet pitfalls that turn a 21-day pre-approval into a 60-day scramble.

Whether you're buying your first home in Loudoun County, refinancing a townhouse in Silver Spring, or relocating to DC for a federal job, having your paperwork organized before you start the application is the single biggest accelerator of a smooth close.

Why Documentation Drives Your Mortgage Timeline

Modern mortgage underwriting is governed by three federal frameworks: the Ability-to-Repay (ATR) rule, the QM (Qualified Mortgage) standard, and the agency guidelines from Fannie Mae, Freddie Mac, FHA, VA, and USDA. Each of these requires the lender to verify — not assume — your income, assets, debts, and identity.

"Verification" means a paper trail. Underwriters cannot accept your word that you earn $145,000 a year. They need W-2s, tax returns, pay stubs, and a verification of employment from your HR department. They cannot accept that the $32,000 in your savings account is yours. They need 60 days of statements showing where it came from.

Every document on the checklist below exists because a federal regulator, an agency guideline, or an investor's overlay requires it. The faster you provide each piece, the faster your loan moves.

Free · No Commitment

Start Your Pre-Approval Today

Upload your documents securely through our digital application and get pre-approved in days, not weeks. No cost, no obligation.

Ken Byrne NMLS #187129 · ALCOVA Mortgage LLC NMLS #40508

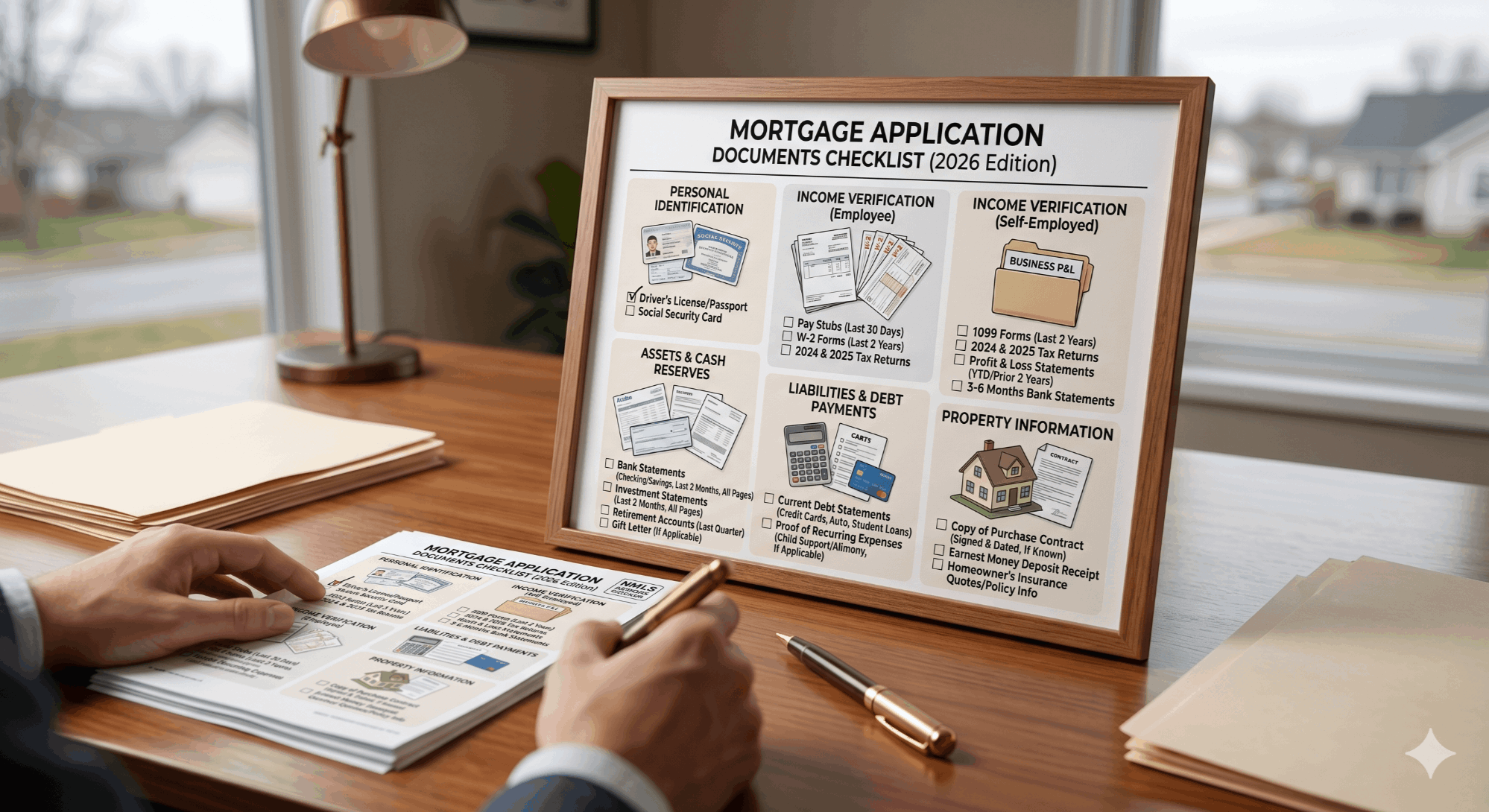

The Master Document Checklist at a Glance

Here is the full list every DMV homebuyer should assemble before — or during the first 48 hours of — a mortgage application. Subsequent sections explain each in detail.

| Category | Documents Required | Coverage Period |

|---|---|---|

| Identification | Driver's license or passport, Social Security number, residence history | Current + 2 years |

| W-2 Income | W-2s, pay stubs, employer contact info, written VOE if requested | 2 years W-2; 30 days stubs |

| Self-Employed | Personal & business tax returns, YTD P&L, business bank statements, K-1s | 2 years + YTD |

| Other Income | Award letters (SS, pension, disability), rental income docs, alimony orders | Current + 2 years |

| Assets | All checking, savings, brokerage, 401(k), IRA statements — every page | 60 days (2 statements) |

| Gift Funds | Signed gift letter, donor's bank statement, transfer evidence | Pre-closing |

| Debts | Student loan statements, child support orders, payoff letters if applicable | Current |

| Property | Signed purchase contract, HOA docs, homeowner's insurance, appraisal access | After contract |

| Special | VA: COE, DD-214 · FHA: CAIVRS clearance · USDA: address eligibility | As applicable |

Personal Identification & Residency

Under the federal Customer Identification Program (CIP) and Patriot Act requirements, every mortgage lender must verify your identity before accepting an application. The documents here are non-negotiable and are usually the easiest part of the file — provided they're current and consistent.

What to Provide

- Government-issued photo ID: Driver's license, state ID, U.S. passport, or military ID. Must be unexpired.

- Social Security number: Provided on the application; physical card is not typically required unless flagged by the credit bureau.

- Two-year residence history: Every address you've lived at, with landlord contact info for any rental periods.

- Marital status documentation: Divorce decree, separation agreement, or property settlement if applicable — even in non-community-property states, alimony and child support orders affect debt-to-income calculations.

- Permanent resident card (if applicable): Non-U.S. citizens need a valid green card or work-authorization documentation; visa-holders may qualify under specific loan programs.

The Hidden Pitfall: Name Mismatches

If your driver's license says "Jonathan Michael Reyes" but your W-2 says "John M. Reyes" and your bank statement says "J. Reyes," underwriting will flag inconsistencies. Provide a one-paragraph letter of explanation, or — if recent — a marriage certificate or court order for legal name changes.

Income Documents for W-2 Employees

For the roughly 80% of DMV borrowers who receive a W-2 from a single employer, income documentation is straightforward. Lenders need to confirm that your earnings are stable, that they will continue for the next three years, and that the pay stubs match what's on your tax return.

Standard W-2 Income Package

- Two most recent years of W-2s from every employer.

- Pay stubs covering 30 days — typically two bi-weekly or four weekly stubs, showing year-to-date earnings.

- Employer name, address, and phone number for the Verification of Employment (VOE).

- Most recent two years of personal federal tax returns, all schedules included — even if W-2-only.

- Written explanation of any employment gaps longer than 30 days within the past two years.

Bonus, Commission, and Overtime Income

Variable income — quarterly bonuses, sales commissions, regular overtime — counts only if there's a documented two-year history. Lenders will average the most recent two years (and sometimes year-to-date) to establish a "usable" monthly figure. A single big year doesn't carry the same weight as a steady two-year track record.

Federal Employees: A DMV Specialty

For the hundreds of thousands of federal workers across Northern Virginia, DC, and the Maryland suburbs, a few specifics apply. SF-50 forms verify position and salary grade. Locality pay is fully countable. Performance awards typically don't qualify unless there's a documented multi-year history. And for borrowers with security clearances who can't disclose employer details, lenders can work from your LES (Leave and Earnings Statement) and base pay schedule.

Income Documents for Self-Employed Borrowers

If you own 25% or more of a business, receive 1099 income, or file a Schedule C, Schedule E, or K-1, you're considered self-employed by mortgage underwriting standards — regardless of how stable your income actually is. The documentation requirement roughly doubles.

Standard Self-Employed Package

- Two years of personal federal tax returns with all schedules (especially Schedule C, E, and SE).

- Two years of business tax returns if you operate as an S-Corp, C-Corp, or partnership (Forms 1120, 1120-S, or 1065).

- Year-to-date Profit & Loss statement, ideally prepared by your CPA, dated within 60 days of application.

- Year-to-date balance sheet for the business if structured as a corporation or partnership.

- Two months of business bank statements — all pages.

- Business license, articles of incorporation, or DBA registration confirming the business has existed for at least two years.

- K-1s for the past two years if you receive partnership or S-Corp distributions.

- 1099-NEC forms from all clients if you're a sole proprietor or independent contractor.

How Lenders Calculate Self-Employed Income

Underwriters use Fannie Mae Form 1084 or Freddie Mac Form 91 to "add back" non-cash expenses — depreciation, amortization, depletion, and (in some cases) one-time losses — to your reported net income. The resulting figure, averaged over two years and divided by 24, becomes your usable monthly income.

If 2024 was strong but 2023 was weak, the two-year average will pull your qualifying income down. If your most recent year is significantly lower than the previous year, underwriting may use only the lower figure. This is the single biggest source of frustration for self-employed buyers, and the reason your CPA's tax strategy matters: aggressive deductions reduce taxable income, which is exactly what's used to qualify you for a mortgage.

Run the Numbers

See What You Can Afford

Estimate your monthly payment for any home price in Virginia, Maryland, or DC before you submit a single document.

Asset & Bank Statement Documentation

Lenders verify assets for two reasons: to confirm you have enough money to cover the down payment, closing costs, and reserves, and to confirm that money is legitimately yours. The standard documentation window is the most recent 60 days — typically two consecutive monthly statements per account.

Accounts You'll Need to Document

- Checking accounts — every account, every page (yes, even the blank ones).

- Savings and money market accounts

- Brokerage accounts — stocks, ETFs, mutual funds; vested portion is typically usable.

- 401(k), 403(b), TSP, and IRA statements — even if you're not withdrawing, lenders count a portion as reserves.

- Health Savings Accounts (HSAs) if used as a savings vehicle.

- Crypto holdings — usable only after liquidating to a U.S. bank account and seasoning the funds.

The "Every Page" Rule

If your bank statement says "Page 1 of 7," underwriting needs pages 1 through 7 — even pages with only "This page intentionally left blank" or fine-print disclosures. Missing pages are the #1 cause of conditional approval delays.

Large Deposits: The 50% Rule

Per Fannie Mae and Freddie Mac guidelines, any non-payroll deposit larger than approximately 50% of your gross monthly income must be sourced and documented. If you earn $8,000 per month and your account shows a $5,200 deposit that didn't come from your employer, underwriting will ask: where did that come from?

Acceptable sourcing: tax refund (provide IRS confirmation), proceeds from selling a car (bill of sale plus title transfer), bonus from work (provide pay stub matching), or a transfer from another disclosed account. Unacceptable: "It was a loan from my brother" with no paper trail.

Down Payment Sourcing & Gift Funds

The federal Anti-Money Laundering rules and agency guidelines require lenders to confirm that every dollar going toward the down payment is from an acceptable source. Acceptable means: your own savings (with 60+ days of seasoning), proceeds from selling an asset, an approved gift from a documented donor, or down payment assistance from an approved agency.

If Your Down Payment is From Personal Savings

As long as the funds have been in your account for at least 60 days, they're considered "seasoned" and require no additional sourcing beyond the standard bank statements.

If Your Down Payment Includes Gift Funds

Gifts from immediate family, a fiancé(e), domestic partner, or in some cases an employer are allowed on virtually every loan program. But the documentation requirement is strict:

- Signed gift letter stating the donor's name, relationship, dollar amount, the property address, and a declaration that the funds are a gift with no expectation of repayment.

- Donor's bank statement showing the funds were in their account before transfer.

- Evidence of transfer — wire confirmation, canceled check, or deposit receipt — showing the funds moving from donor to borrower.

If Your Down Payment Includes DPA Assistance

DMV homebuyers using Virginia Housing's Down Payment Assistance Grant, the Maryland Mortgage Program (MMP), or DC's Home Purchase Assistance Program (HPAP — up to $202,000) will need program-specific paperwork from the administering agency in addition to the standard checklist. Your lender coordinates this directly with the DPA provider — your job is to complete the homebuyer education course and submit the agency's application package on time.

Debt & Credit Documentation

Most of your debt information is pulled directly from your credit report. But certain situations require additional documentation, especially anything that affects your debt-to-income ratio.

Documents Required When Applicable

- Student loan statements showing balance, payment, and repayment plan (especially important for income-driven repayment plans, which are calculated differently across loan programs).

- Child support or alimony orders if you pay or receive support — affects DTI in both directions.

- Court orders or judgments for any liens, judgments, or settlements showing on the credit report.

- Bankruptcy discharge papers if you've filed Chapter 7 or 13 within the past seven years.

- Letters of explanation for credit inquiries within the past 90 days, late payments within the past 24 months, or collection accounts.

- Payoff statements for any debts you plan to pay off before or at closing.

The Letter of Explanation (LOE)

Lenders are required by federal regulation to investigate "derogatory" credit items. Your job — through a brief signed letter — is to provide context: a medical bill that went to collections after an insurance dispute, a late payment during a job transition, a credit inquiry from refinancing a car. Keep these letters factual, brief, and honest.

Free · No Commitment

Get Pre-Approved Before Document Stress Sets In

Our secure portal walks you through every document upload step-by-step. Start today and know your buying power before the weekend.

Ken Byrne NMLS #187129 · ALCOVA Mortgage LLC NMLS #40508

Property Documents (After You're Under Contract)

Once you're pre-approved and a seller accepts your offer, a new layer of documentation kicks in. These items relate to the property itself, not to you as a borrower.

- Fully ratified purchase contract — signed by all parties, with all addenda.

- Earnest money deposit (EMD) receipt — canceled check or wire confirmation.

- HOA or condo association documents — bylaws, budget, master insurance policy declarations, and resale disclosure (especially critical for condos, which must be on the lender's approved-project list or individually approved).

- Homeowner's insurance binder — secured before closing, with the lender named on the mortgagee clause.

- Termite/WDI inspection report (required on VA loans, often required by Virginia and Maryland purchase contracts regardless).

- Appraisal access — the lender orders this; you don't provide it, but you'll pay the fee at closing or at appraisal scheduling.

- Flood determination — if the property is in a FEMA flood zone, flood insurance is required.

DMV-Specific Property Document Notes

Northern Virginia condo buyers in Reston, Tysons, Ballston, and Old Town Alexandria should expect a longer condo questionnaire process. Many high-rise buildings require individual project approval through Fannie Mae or FHA, which can add 5–10 days to underwriting.

DC row house buyers often deal with non-warrantable condo classifications in smaller (2–4 unit) buildings, which may require a portfolio loan rather than a conforming product. Your lender should flag this within 48 hours of seeing the contract.

Special Documents by Loan Type (VA, FHA, USDA, Jumbo)

Most documents are universal, but each loan program adds program-specific paperwork.

| Loan Type | Additional Documents Required | 2026 DC Metro Loan Limit |

|---|---|---|

| Conventional | Standard package — no extras for most W-2 buyers | $1,249,125 |

| FHA | CAIVRS clearance, prior-foreclosure waiting period docs | $1,149,825 |

| VA | Certificate of Eligibility (COE), DD-214, current LES (active duty), termite inspection | No limit with full entitlement |

| USDA | Property address eligibility check, household income worksheet | Income-based |

| Jumbo | Larger reserve requirements (6–12 months), often two appraisals, more granular asset sourcing | $1,249,126+ |

VA Loan Specifics for the DMV's Massive Military Market

If you're using VA financing for a home near Fort Belvoir, Quantico, Joint Base Andrews, or the Pentagon, you'll need your Certificate of Eligibility (COE), which your lender can pull through the VA portal in most cases. Active-duty service members provide their current LES. Veterans provide their DD-214. Surviving spouses provide a COE based on the veteran's service record.

Common Documentation Mistakes That Delay Closings

After working with thousands of DMV buyers, the same handful of mistakes account for the bulk of pre-closing scrambles. Knowing them in advance is half the cure.

Submitting screenshots instead of full PDFs

Underwriters need official, downloadable PDFs from the bank's portal — not phone photos and not screen captures. Most banks let you download official statements as PDFs from the "Documents" or "Statements" tab.

Skipping "blank" pages on bank statements

Even if a page only contains disclosures or the "intentionally blank" notice, underwriting needs every numbered page in the statement.

Making large undocumented deposits mid-process

Selling a car? Receiving a tax refund? Getting reimbursed for a work trip? Document it immediately — don't wait for underwriting to ask.

Opening new credit during the application

A new credit card, a financed sofa from Restoration Hardware, or a car loan signed mid-process triggers re-underwriting and can disqualify you. Wait until after closing.

Changing jobs without notifying your lender

Even a lateral move to a higher-paying job at the same kind of company requires re-verification. Tell your loan officer before you accept the offer.

Co-mingling personal and business funds

Self-employed buyers: keep a clean separation. If business funds are used for personal expenses (or vice versa), underwriting will require additional sourcing for every transfer.

When Documents Are Due: The Loan Timeline

Documents aren't required all at once — they're requested in phases. Here's the rough sequence from first application to closing day.

Day 1–3: Application & Initial Document Upload

ID, two years W-2 or tax returns, 30 days of pay stubs, 60 days of bank statements. This package generates your initial pre-approval letter.

Day 4–7: Pre-Approval Letter Issued

Underwriting reviews the file and issues a pre-approval letter with the maximum loan amount you qualify for. Now you can shop with confidence.

Day 8–30: House Shopping & Contract

Once you're under contract, submit the ratified contract, EMD receipt, and any HOA documents within 24–48 hours.

Day 30–40: Conditional Approval & Document Requests

Underwriting issues a "conditional approval" — a list of remaining documents needed. Most are clarifications: updated bank pages, LOEs for inquiries, gift letter packages.

Day 40–45: Clear to Close (CTC)

All conditions met. Your insurance binder is in, appraisal is back at value, and the file is ready for closing disclosure.

Day 45+: Closing Day

You bring ID and a cashier's check or wire confirmation for the final amount listed on the Closing Disclosure. Sign the deed and the promissory note. Keys are yours.

Ready to Start Your Search?

Browse Homes for Sale in Northern Virginia

Once your documents are in order and you're pre-approved, explore available homes across Loudoun, Fairfax, Prince William, Arlington, and Alexandria.

Putting It All Together

A mortgage application is paperwork-heavy, but it's also entirely predictable. The borrowers who close on time and on budget are the ones who treat the document collection process like a project: they gather the standard package before starting, they respond to lender requests within 24 hours, and they avoid the major financial moves — new credit, undocumented deposits, job changes — that derail otherwise-strong files.

If you're also planning to sell your current home as part of the move, an integrated buy-sell strategy can save tens of thousands in commission and reduce the timing pressure of contingent offers. Many DMV buyers don't realize they can list their existing home at a reduced commission rate while financing their next purchase through the same coordinated team.

Pull your two most recent pay stubs, your last two bank statements, and your last two W-2s right now. That's roughly 60% of the standard application package. Doing that this afternoon will save you days of back-and-forth later.

Selling & Buying Together?

Save Thousands With a 1.5% Listing

If you're selling your current home as part of your move, explore a full-service listing program at a reduced commission — keep more of your equity to put toward your next home.

Frequently Asked Questions

What documents do I need for a mortgage application in 2026?

The standard package includes: government-issued photo ID, two years of W-2s or full tax returns, 30 days of pay stubs, 60 days of bank and asset statements (every page), residence history for two years, and signed letters of explanation for any credit inquiries, employment gaps, or large deposits. Self-employed borrowers add personal and business tax returns, a YTD profit and loss statement, and business bank statements.

Do I need to provide tax returns if I'm a W-2 employee?

Most W-2 employees with single-employer income and no other income sources can qualify with W-2s and pay stubs alone (called a "W-2 only" file). However, if you have rental income, side business income, K-1 income, or significant unreimbursed business expenses, full tax returns are required. Many lenders request returns regardless, as a precaution.

How many months of bank statements do I need for a mortgage in Virginia?

The standard requirement across Virginia, Maryland, and DC is two consecutive monthly statements covering 60 days — every page, every account where you hold funds being used for the down payment, closing costs, or reserves. Some loan programs (jumbo, some portfolio products) may require 90 days or three statements.

What is the 50% deposit rule in mortgage underwriting?

Under Fannie Mae and Freddie Mac guidelines, any non-payroll deposit larger than approximately 50% of your gross monthly income must be sourced and documented. If you earn $10,000 a month and a $6,000 deposit appears in your bank statements, you'll need to show where it came from — a tax refund, asset sale, transfer from a disclosed account, or other documented source.

Can I use gift funds for my down payment in the DMV?

Yes. Gift funds from immediate family, a fiancé(e), or a domestic partner are allowed on conventional, FHA, and VA loans. You'll need a signed gift letter, the donor's most recent bank statement showing the funds were in their account, and evidence of the transfer (wire confirmation or canceled check).

What documents do self-employed borrowers need for a mortgage?

Self-employed borrowers need two years of personal federal tax returns with all schedules, two years of business returns (for S-Corps, C-Corps, or partnerships), a year-to-date profit and loss statement, two months of business bank statements, the business license or articles of incorporation, K-1s if applicable, and 1099-NEC forms for sole proprietors.

What is the conforming loan limit for the DC metro area in 2026?

For 2026, the conforming loan limit for the DC metro high-cost area is $1,249,125 for a single-family home. The FHA loan limit for the DC metro area is $1,149,825. These limits apply to most of Northern Virginia, the Maryland suburbs of DC, and the District of Columbia itself.

What additional documents do VA loan borrowers need?

VA loan borrowers need a Certificate of Eligibility (COE), which the lender can typically pull through the VA portal. Active-duty service members provide a current Leave and Earnings Statement (LES). Veterans provide their DD-214 discharge papers. Surviving spouses provide a COE issued based on the veteran's service. A termite inspection is also required on every VA-financed purchase.

How do I get pre-approved for a mortgage in Northern Virginia?

Start by completing an online application with a licensed lender, then upload your initial document package (ID, W-2s, pay stubs, bank statements). Most lenders, including ALCOVA Mortgage, can issue a pre-approval letter within 3–5 business days once a complete file is in. You can begin your application securely at apply.alcova.com.

What is a Letter of Explanation (LOE) and when is one required?

A Letter of Explanation is a brief signed statement clarifying anything in your file that might raise underwriting questions: recent credit inquiries, late payments, employment gaps, large deposits, name discrepancies, or address changes. Keep it factual and short — two or three sentences is usually enough.

How do I find a good mortgage lender in the DMV?

Look for a licensed lender with deep DMV experience, transparent pricing, and responsive communication. Verify NMLS credentials through the NMLS Consumer Access database. Ken Byrne, NMLS #187129, works through ALCOVA Mortgage LLC (NMLS #40508) and is licensed across Virginia, Maryland, DC, and West Virginia — a useful footprint for buyers crossing state lines for work or relocation.

How long are mortgage documents valid before they need to be updated?

Most income and asset documents have a 60-day shelf life — pay stubs older than 30 days at closing, bank statements older than 60 days, and credit reports older than 120 days will need to be refreshed before closing. If your file sits in pre-approval for several months while you shop, expect to provide updated paperwork once you go under contract.

Glossary of Mortgage Document Terms

CAIVRS: Credit Alert Verification Reporting System. A federal database checked for FHA, VA, and USDA loans to confirm the borrower has no past defaults on federal debt.

Certificate of Eligibility (COE): The VA-issued document confirming a service member's eligibility for VA home loan benefits.

Conditional Approval: The stage of underwriting where the loan is approved subject to specific outstanding items being cleared (updated paperwork, appraisal, insurance binder, etc.).

DTI (Debt-to-Income Ratio): The percentage of your gross monthly income that goes to all monthly debt payments, including the new mortgage.

Gift Letter: A signed statement from a donor confirming that funds provided to the borrower are a gift, not a loan, with no expectation of repayment.

LOE (Letter of Explanation): A brief signed statement from the borrower clarifying anomalies in the file — credit inquiries, employment gaps, address mismatches, large deposits.

Seasoned Funds: Money that has been in the borrower's account for at least 60 days, requiring no additional sourcing documentation.

VOE (Verification of Employment): A written or verbal confirmation from the borrower's employer that confirms job title, length of employment, and income.

Disclaimer: This article is for informational purposes only and does not constitute financial or legal advice. Mortgage programs, rates, and eligibility requirements are subject to change. Contact a licensed mortgage professional for guidance specific to your situation. Ken Byrne, NMLS #187129 · ALCOVA Mortgage LLC, NMLS #40508 · Licensed in VA, MD, DC, WV.

Categories

Recent Posts

GET MORE INFORMATION

Broker Associate