FHA Loan Limits in Maryland 2026

FHA Loan Limits in Maryland 2026: Your County-by-County Guide

By Ken Byrne, NMLS #187129 · ALCOVA Mortgage LLC, NMLS #40508 · Updated May 2026

Quick Answer: For 2026, FHA loan limits in Maryland range from $541,287 in lower-cost counties to $1,249,125 in the five Washington-metro counties (Montgomery, Prince George's, Frederick, Charles, and Calvert). Your exact limit depends on which county the home is in — Baltimore-area counties fall in a mid-tier between those two figures. FHA loans require as little as 3.5% down with a 580 credit score.

Key Takeaways

- The 2026 range: $541,287 (floor) to $1,249,125 (ceiling) for a single-family home in Maryland.

- Five high-cost counties: Montgomery, Prince George's, Frederick, Charles, and Calvert all qualify for the full $1,249,125 ceiling.

- Most counties use the floor: The majority of Maryland's 24 counties are capped at $541,287.

- Limits scale up for multi-unit homes: A 4-unit property in a high-cost county can reach roughly $2.4 million.

- Qualifying basics: 3.5% down with a 580+ score, or 10% down with a 500–579 score.

- Limits ≠ approval: The loan limit caps borrowing; your income, debts, and credit determine what you actually qualify for.

Table of Contents

- What FHA Loan Limits Are (and How They're Set)

- Maryland's 2026 FHA Loan Limits

- County-by-County Breakdown

- Multi-Unit Property Limits

- FHA Qualifying Requirements in Maryland

- Loan Limit vs. What You'll Actually Get Approved For

- FHA vs. Conventional in Maryland

- What If Your Home Is Over the FHA Limit?

- How to Apply: Step by Step

- Common FHA Mistakes to Avoid

- Frequently Asked Questions

- Glossary

If you're buying a home in Maryland with an FHA loan, the single most important number to know before you start shopping is your county's FHA loan limit. It's the maximum the Federal Housing Administration will insure on a mortgage in your area — and in a state as economically split as Maryland, that number swings dramatically. A buyer in Montgomery County can borrow more than double what a buyer in Garrett County can with the same loan program.

This matters because Maryland straddles two very different housing economies: the high-cost Washington, D.C. suburbs in the central and southern part of the state, and far more affordable markets out west and on the Eastern Shore. The FHA limit is calibrated to that local reality. Below, we'll walk through exactly what your 2026 limit is, how the FHA sets it, and — just as important — why hitting the limit doesn't automatically mean you'll be approved for that amount.

What FHA Loan Limits Are (and How They're Set)

An FHA loan limit is the largest mortgage the Federal Housing Administration will insure on a property in a given county. If you need to borrow more than the limit, you can't use a standard FHA loan for that purchase — you'd need a conventional loan, a jumbo loan, or a larger down payment to bring the financed amount under the cap.

These limits aren't arbitrary. Each year, the Federal Housing Finance Agency (FHFA) sets a national conforming loan limit based on home-price changes. For 2026, that baseline is $832,750. The FHA then builds its own limits around two anchors tied to that baseline:

- The "floor" — 65% of the conforming baseline, which equals $541,287 for 2026. This applies to most lower-cost counties.

- The "ceiling" — 150% of the conforming baseline, which equals $1,249,125 for 2026. This applies to designated high-cost areas, including the D.C. metro counties.

Counties whose local median home price lands between those two anchors get a limit somewhere in the middle, calculated from area median prices. That's why Maryland has three effective tiers: floor counties, a mid-tier Baltimore-area group, and the high-cost ceiling counties around Washington.

Maryland's 2026 FHA Loan Limits

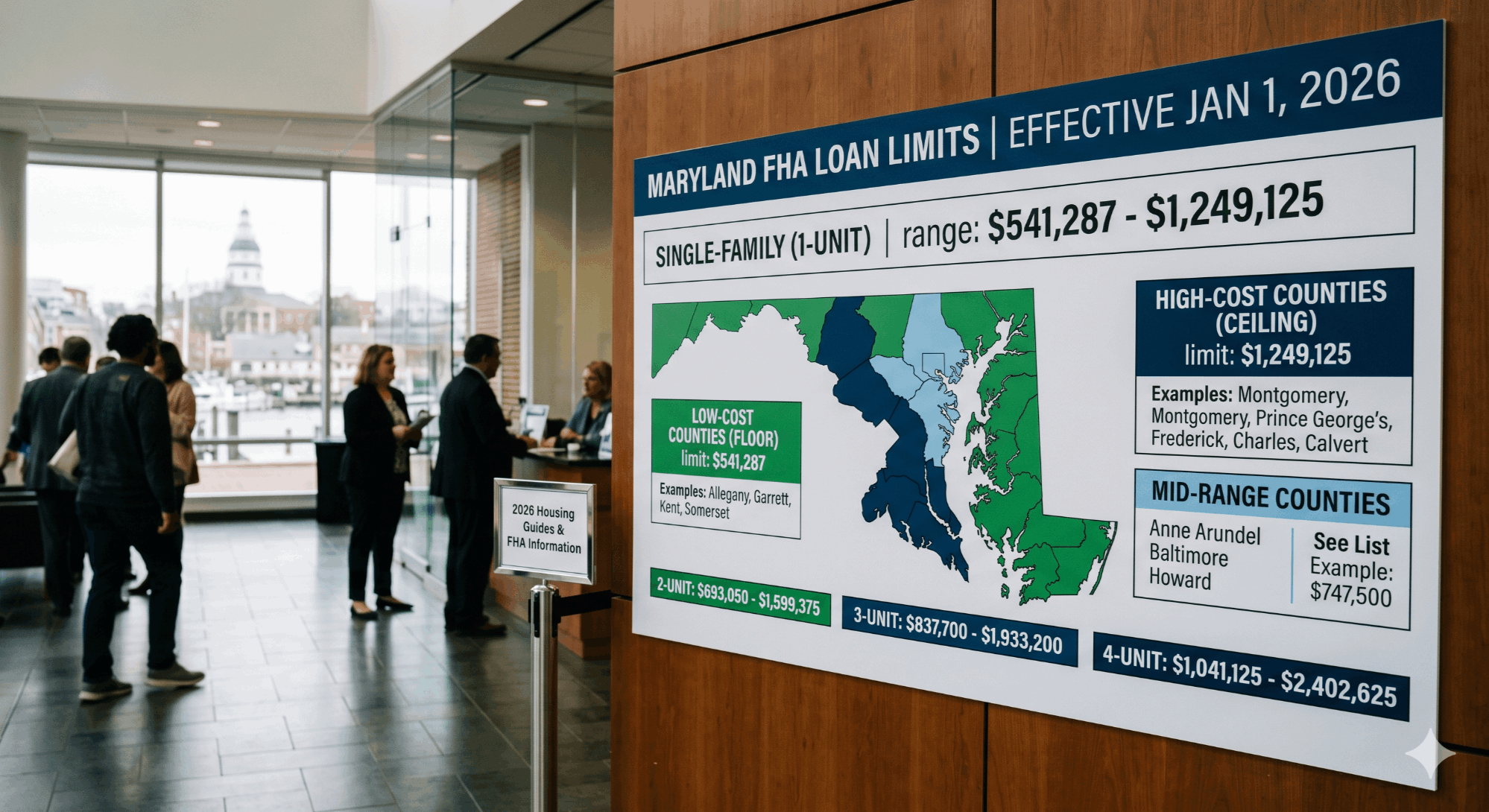

Here's the quick version: for a single-family home in 2026, Maryland FHA limits run from $541,287 at the low end to $1,249,125 at the high end. Where your county lands depends almost entirely on its proximity to Washington, D.C.

2026 FHA Single-Family Limit by Tier

Floor counties (most of Maryland) — $541,287

Baltimore-area mid-tier — between $541,287 and $1,249,125

High-cost D.C. metro counties — $1,249,125

The five Maryland counties that sit inside the Washington, D.C. high-cost metro area — Montgomery, Prince George's, Frederick, Charles, and Calvert — all receive the full ceiling of $1,249,125. That's the same limit as Washington, D.C. itself and the high-cost Northern Virginia counties, because HUD treats the entire D.C. metro as one high-cost zone.

Most of Maryland's remaining counties — including the Eastern Shore and western Maryland — are capped at the $541,287 floor. The Baltimore-Columbia-Towson area counties (such as Anne Arundel, Baltimore County, Howard, Carroll, Harford, and Queen Anne's) fall into a mid-tier limit set above the floor but below the ceiling, because the Baltimore metro's median home price is higher than rural Maryland but lower than the D.C. suburbs.

Local accuracy note: Because the Baltimore mid-tier figure is recalculated annually from area median prices, always confirm your exact county limit with your lender or HUD's official FHA Mortgage Limits lookup tool before making an offer — national sites frequently publish the prior year's number.

Free · No Commitment

See What You Qualify For Today

Get pre-approved in minutes and know exactly how much home you can afford with an FHA loan anywhere in Maryland. No cost, no obligation.

Ken Byrne NMLS #187129 · ALCOVA Mortgage LLC NMLS #40508

County-by-County Breakdown

The table below groups Maryland's counties by their 2026 FHA single-family tier. Counties in the high-cost group share the D.C. metro ceiling; counties in the floor group share the statewide minimum.

| Tier | Counties | 2026 1-Unit FHA Limit |

|---|---|---|

| High-cost (D.C. metro) | Montgomery, Prince George's, Frederick, Charles, Calvert | $1,249,125 |

| Baltimore-area mid-tier | Anne Arundel, Baltimore County, Baltimore City, Howard, Carroll, Harford, Queen Anne's | Between floor & ceiling — confirm with lender |

| Floor (lower-cost) | Allegany, Garrett, Washington, Cecil, Caroline, Dorchester, Kent, Somerset, St. Mary's, Talbot, Wicomico, Worcester | $541,287 |

A practical takeaway: if you're buying in Montgomery or Prince George's County — Maryland's two most populous D.C.-suburb counties — you have well over $1.2 million of FHA borrowing power, which covers the large majority of homes in those markets. If you're buying on the Eastern Shore or in western Maryland, the $541,287 floor is still more than enough for the typical home price in those areas.

Multi-Unit Property Limits

FHA limits aren't just for single-family homes. The program allows you to finance two-, three-, and four-unit properties — a popular "house hacking" strategy where you live in one unit and rent out the others. Multi-unit limits are fixed multiples of the single-family limit, so they're substantially higher.

| Units | Floor Counties | High-Cost D.C. Metro Counties |

|---|---|---|

| 1 unit | $541,287 | $1,249,125 |

| 2 units | ~$692,900 | ~$1,599,000 |

| 3 units | ~$837,500 | ~$1,933,000 |

| 4 units | ~$1,040,500 | ~$2,402,625 |

The catch with multi-unit FHA financing: you must occupy one of the units as your primary residence for at least a year, and you move in within 60 days of closing. The upside is that lenders can count a portion of the projected rental income from the other units toward your qualifying income, which can meaningfully increase how much home you can afford.

Run the Numbers

What Will Your Monthly Payment Be?

Use our mortgage calculator to estimate your FHA monthly payment — including mortgage insurance — for any home price in Maryland.

FHA Qualifying Requirements in Maryland

FHA guidelines are federal — they're identical in Maryland, Virginia, D.C., and everywhere else. Only the loan limit changes by location. Here are the core qualifying standards:

| Requirement | FHA Standard |

|---|---|

| Minimum credit score | 580 for 3.5% down; 500–579 for 10% down |

| Minimum down payment | 3.5% (or 10% with a 500–579 score) |

| Debt-to-income ratio | Often up to 57% with strong compensating factors; many lenders cap lower |

| Mortgage insurance | 1.75% upfront premium + annual premium (≈0.15%–0.75%) |

| Occupancy | Must be a primary residence (no pure investment properties) |

| Appraisal | FHA appraisal with minimum property standards |

One Maryland-specific resource worth knowing: if student loan debt is pushing your debt-to-income ratio too high, the Maryland SmartBuy 3.0 program can provide up to $20,000 in student debt relief for qualifying buyers, which can be paired with an FHA loan to help you qualify.

Loan Limit vs. What You'll Actually Get Approved For

This is the single biggest misunderstanding about loan limits. The FHA limit is a ceiling, not a promise. Just because Montgomery County allows up to $1,249,125 doesn't mean you'll be approved for that amount. Your real approval is driven by three personal factors:

- Income: Your gross monthly income sets the outer boundary of what you can repay.

- Debt-to-income ratio: Existing debts (car loans, student loans, credit cards) reduce how much mortgage you can carry.

- Credit and reserves: Your score affects rate and approval; some files need cash reserves after closing.

In practice, most Maryland FHA buyers are approved for far less than their county's ceiling — the limit rarely becomes the binding constraint unless you're buying a high-priced home in a floor county. The number that actually matters for your search is your personal pre-approval amount, which is why getting pre-approved before you shop is the most useful first step you can take.

FHA vs. Conventional in Maryland

In high-cost Maryland counties, the FHA ceiling and the conventional baseline are very close, so the choice usually comes down to credit and down payment rather than loan size:

| Factor | FHA | Conventional |

|---|---|---|

| Min. credit score | 500–580 | 620+ |

| Min. down payment | 3.5% | 3%–5% |

| Mortgage insurance | Upfront + annual (often for life of loan) | PMI, removable at 20% equity |

| DC-metro limit (2026) | $1,249,125 | $1,249,125 |

| Best for | Lower credit / smaller down payment | Stronger credit, avoiding lifetime MI |

A common Maryland strategy: use FHA to get into the home now if your credit is in the 580–660 range, then refinance into a conventional loan once your score and equity improve to drop mortgage insurance. A local lender can model whether that path saves you money over your expected time in the home.

Selling While You Buy?

Keep More of Your Equity at 1.5%

If you're selling a current home to buy your next one, a full-service 1.5% listing program can preserve thousands in equity to put toward your down payment.

What If Your Home Is Over the FHA Limit?

If the home you want exceeds your county's FHA limit, you still have options. You don't have to abandon the purchase — you just need a different structure:

- Increase your down payment: Putting more down lowers the financed amount; if it falls under the FHA limit, FHA is back on the table.

- Switch to a conventional loan: In high-cost Maryland counties the conventional limit matches the FHA ceiling, so this often solves the problem outright.

- Use a jumbo loan: For homes above the conforming ceiling, a jumbo loan covers the gap — typically requiring stronger credit and reserves.

This is exactly the kind of scenario where talking to a lender early pays off. Identifying the right product on day one — rather than after an offer is accepted — keeps your timeline on track and your offer competitive.

How to Apply: Step by Step

Check your county's limit. Confirm the 2026 FHA limit for the county where you'll buy so you know your ceiling before shopping.

Review your credit. Pull your scores and address any errors — 580 unlocks the 3.5% down option.

Gather documents. Two years of W-2s/tax returns, recent pay stubs, and bank statements.

Get pre-approved. A lender verifies income and debts and issues your true buying number.

Shop and make an offer. Stay within your pre-approval and your county's FHA limit.

Appraisal and underwriting. The FHA appraisal confirms value and property condition before final approval.

Close. Sign final documents, pay closing costs, and take ownership.

Ready to Start Your Search?

Browse Homes for Sale in Maryland & the DMV

Once you know your FHA budget, explore available homes across Montgomery, Prince George's, Frederick, and the wider DMV.

Common FHA Mistakes to Avoid

- Assuming the limit is your budget. Your pre-approval amount, not the county ceiling, is what you can actually spend.

- Using last year's numbers. Limits reset annually — many websites lag a full year behind.

- Forgetting mortgage insurance. FHA's upfront and annual premiums add real cost; factor them into your monthly estimate.

- Making large deposits before closing. Unexplained deposits can delay underwriting; document the source of all funds.

- Taking on new debt mid-process. A new car loan or credit card can push your DTI over the line right before closing.

- Skipping pre-approval. In competitive DMV markets, offers without a solid pre-approval rarely win.

Putting It All Together

Maryland's 2026 FHA loan limits reflect the state's split housing economy: a high-cost ceiling of $1,249,125 in the five Washington-metro counties, a $541,287 floor across most of the state, and a Baltimore-area mid-tier in between. Knowing your county's number is the foundation, but the more important number is your personal pre-approval — that's what determines the homes you can realistically pursue.

If you're weighing an FHA loan in Maryland, the most productive next step is a no-cost pre-approval. It converts the abstract county limit into a concrete buying number and positions you to move quickly when the right home appears.

Free · No Commitment

Find Out Your Real FHA Buying Power

Get pre-approved with a local Maryland mortgage expert and turn your county's FHA limit into a clear, personalized number.

Ken Byrne NMLS #187129 · ALCOVA Mortgage LLC NMLS #40508

Frequently Asked Questions

What is the FHA loan limit in Maryland for 2026?

For 2026, single-family FHA loan limits in Maryland range from $541,287 in lower-cost counties to $1,249,125 in the five Washington-metro counties (Montgomery, Prince George's, Frederick, Charles, Calvert). Baltimore-area counties fall in a mid-tier between those figures.

What is the FHA loan limit in Montgomery County, Maryland?

Montgomery County sits inside the high-cost Washington, D.C. metro area, so its 2026 single-family FHA limit is the full ceiling of $1,249,125 — the same as Prince George's, Frederick, Charles, and Calvert counties.

What credit score do I need for an FHA loan in Maryland?

A credit score of 580 or higher qualifies you for the minimum 3.5% down payment. Scores between 500 and 579 may still qualify but require at least 10% down. Lender overlays sometimes set a higher minimum than 580.

How much down payment do I need for an FHA loan in Maryland?

The minimum is 3.5% of the purchase price with a 580+ score. On a $400,000 home that's $14,000. Down payment assistance and gift funds from family are permitted under FHA rules.

Does the FHA loan limit mean I'll be approved for that amount?

No. The limit is a maximum, not a guarantee. Your actual approval depends on income, debt-to-income ratio, credit, and reserves. Most buyers are approved for considerably less than their county's ceiling.

What is the FHA loan limit in Prince George's County for 2026?

Prince George's County is part of the D.C. high-cost metro, so its 2026 single-family FHA limit is $1,249,125 — well above the median home price there, which gives most buyers ample borrowing room.

Can I use an FHA loan for a multi-unit property in Maryland?

Yes. FHA finances 2–4 unit properties with higher limits, reaching roughly $2.4 million for a 4-unit home in high-cost counties. You must live in one unit as your primary residence for at least a year.

What are the closing costs for an FHA loan in Maryland?

Maryland FHA closing costs typically run 2%–5% of the loan amount and include the 1.75% upfront mortgage insurance premium, lender fees, title work, recordation and transfer taxes, and prepaid escrows. Sellers can contribute toward these costs under FHA rules.

How do I get pre-approved for an FHA loan in Maryland?

Submit recent pay stubs, two years of tax returns or W-2s, and bank statements to a licensed lender, who will verify your income and debts and issue a pre-approval letter showing your true buying number. You can start a no-cost application online with ALCOVA Mortgage.

Is the FHA limit different from the conventional loan limit in Maryland?

In high-cost D.C.-metro counties they're effectively the same ($1,249,125 for 2026). In lower-cost counties the FHA floor ($541,287) is below the conventional baseline ($832,750), so conventional can allow a larger loan in those areas.

Does Maryland have programs to help with FHA down payments?

Yes. The Maryland Mortgage Program (MMP) offers down payment and closing-cost assistance that can pair with FHA financing, and Maryland SmartBuy 3.0 provides up to $20,000 in student debt relief for eligible buyers.

How do I find a good FHA mortgage lender in Maryland?

Look for a lender licensed in Maryland with FHA experience, transparent fee disclosure, and strong local market knowledge. Ken Byrne (NMLS #187129) with ALCOVA Mortgage LLC (NMLS #40508) is licensed in VA, MD, DC, and WV and works with FHA buyers throughout the DMV.

Glossary

FHA Loan: A mortgage insured by the Federal Housing Administration, designed for buyers with lower credit scores or smaller down payments.

Loan Limit: The maximum loan amount the FHA will insure in a given county; varies by location and resets annually.

Floor: The minimum FHA limit, set at 65% of the national conforming baseline — $541,287 for 2026.

Ceiling: The maximum FHA limit, set at 150% of the conforming baseline — $1,249,125 for 2026, applied to high-cost areas.

Conforming Loan Limit: The baseline mortgage amount set annually by the FHFA; $832,750 nationally for 2026.

Mortgage Insurance Premium (MIP): FHA's required insurance — a 1.75% upfront charge plus an annual premium added to the monthly payment.

Debt-to-Income (DTI) Ratio: The share of gross monthly income spent on debt payments; a key approval factor.

Pre-Approval: A lender's conditional commitment stating how much you can borrow, based on verified income, credit, and debts.

Disclaimer: This article is for informational purposes only and does not constitute financial or legal advice. Mortgage programs, rates, and eligibility requirements are subject to change. Multi-unit limit figures shown are approximate; confirm exact county and property-specific limits with a licensed lender or HUD's official FHA Mortgage Limits tool. Contact a licensed mortgage professional for guidance specific to your situation. Ken Byrne, NMLS #187129 · ALCOVA Mortgage LLC, NMLS #40508 · Licensed in VA, MD, DC, WV.

Categories

Recent Posts

GET MORE INFORMATION

Broker Associate