FHA Loan Limits in Northern Virginia 2026

FHA Loan Limits in Northern Virginia 2026

By Ken Byrne, NMLS #187129 · ALCOVA Mortgage LLC, NMLS #40508 · Updated May 2026

Quick Answer: For 2026, the FHA loan limit for a single-family home across all of Northern Virginia is $1,149,825. Every Northern Virginia jurisdiction — Fairfax, Loudoun, Prince William, Arlington, Alexandria, Falls Church, and the rest — sits inside the Washington-Arlington-Alexandria high-cost metro area, so they all share this same FHA ceiling. Multi-unit properties (2–4 units) qualify for higher limits, and you can still buy with as little as 3.5% down with a 580 credit score.

Key Takeaways

- $1,149,825 is the 2026 FHA limit for a 1-unit home everywhere in Northern Virginia — there is no county-by-county variation within the DC metro.

- Multi-unit limits are higher: up to $2,211,600 for a 4-unit property, useful for house-hacking owner-occupants.

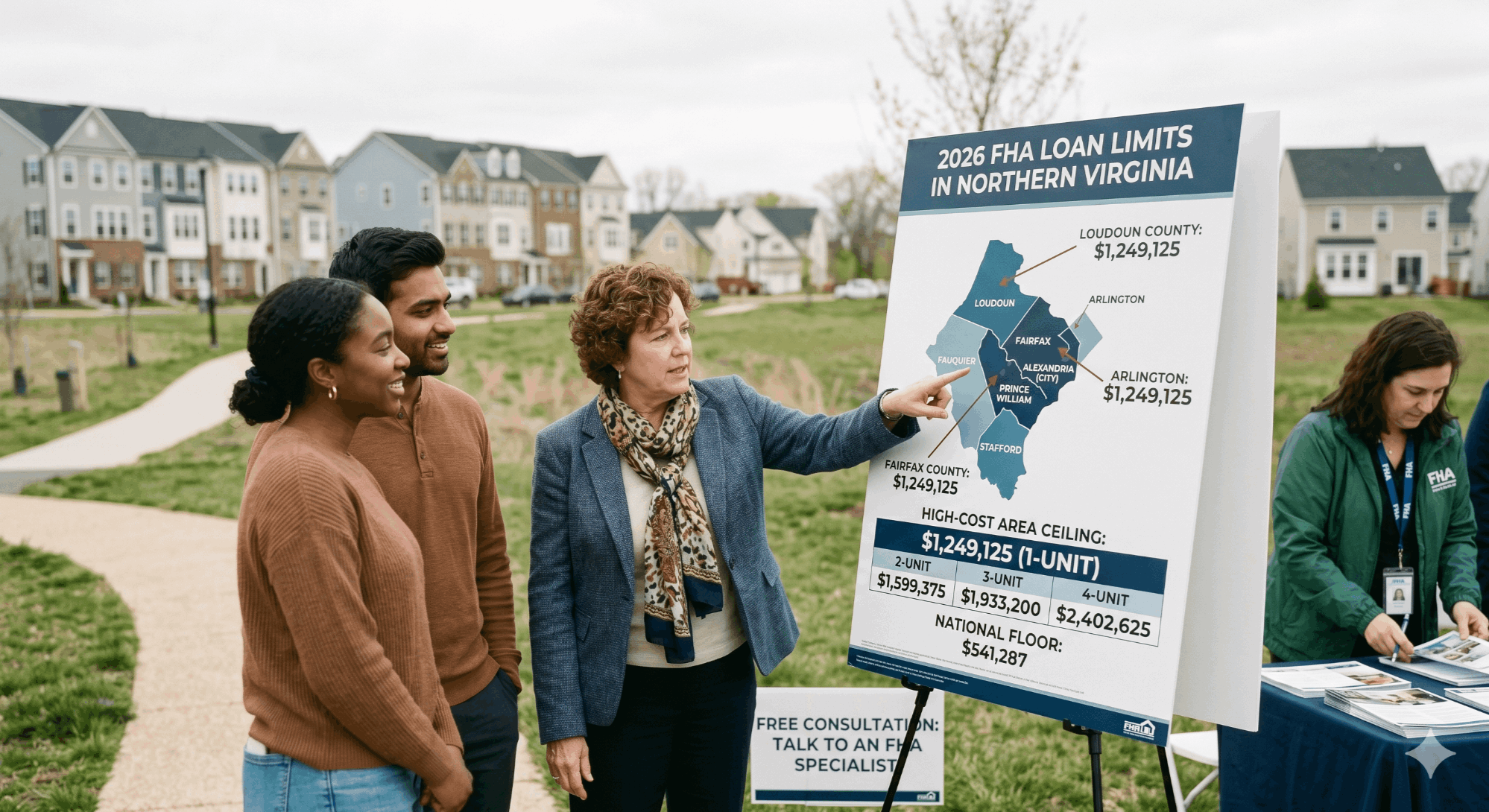

- FHA vs. conforming: the 2026 high-cost conforming limit is $1,249,125 — slightly above the FHA ceiling, so the loan type that fits depends on your credit and down payment, not just price.

- Down payment: as low as 3.5% with a 580+ FICO; 10% required between 500–579.

- Mortgage insurance is required on every FHA loan regardless of down payment — budget for both the upfront and annual premiums.

- Above the limit? A jumbo or high-balance conventional loan is the alternative for Northern Virginia's higher price points.

Table of Contents

- What FHA Loan Limits Are — and Why They Matter

- 2026 FHA Loan Limits for Northern Virginia

- FHA Limits by Northern Virginia County

- How FHA Loan Limits Are Calculated

- FHA vs. Conforming vs. Jumbo in NOVA

- Down Payment & Credit Requirements

- Who Should Use an FHA Loan in Northern Virginia

- How to Get an FHA Loan in Northern Virginia

- Common FHA Mistakes to Avoid

- The Bottom Line for NOVA Buyers

- Frequently Asked Questions

- Glossary

If you're shopping for a home in Northern Virginia and considering an FHA loan, the single most important number to understand is the loan limit — the maximum amount the Federal Housing Administration will insure for a mortgage in your area. Get this number wrong and you can waste weeks chasing homes that won't fit the financing, or assume you're priced out when you actually aren't.

Here's the good news: Northern Virginia sits in one of the highest-cost metro areas in the country, which means the FHA limit here is far higher than the national baseline. A buyer in rural Virginia might be capped near $524,000, but in Fairfax, Loudoun, or Arlington, the FHA ceiling for a single-family home in 2026 is $1,149,825.

This guide breaks down exactly what that means for you — the limits by property type, how they compare to conforming and jumbo loans, what you actually need to qualify, and how to move forward if your target home sits above the line.

What FHA Loan Limits Are — and Why They Matter

An FHA loan is a mortgage insured by the Federal Housing Administration, part of the U.S. Department of Housing and Urban Development (HUD). Because the government insures the loan against default, lenders can offer easier credit requirements and lower down payments than a conventional mortgage. That makes FHA financing one of the most popular paths for first-time buyers and anyone with a thinner credit file.

The FHA loan limit is the maximum loan amount FHA will insure for a property of a given size in a given county. It is not a price cap on the home itself — you can buy a home that costs more than the limit — but FHA will only insure up to the limit, so any amount above it would need to come from a larger down payment or a different loan product entirely.

FHA limits are recalculated every year and are tied directly to the conforming loan limit set by the Federal Housing Finance Agency (FHFA). In high-cost regions like the Washington, D.C. metro, the limit is set well above the national floor to reflect local home prices. This is why Northern Virginia buyers have substantially more FHA buying power than buyers in most of the country.

2026 FHA Loan Limits for Northern Virginia

All of Northern Virginia falls within the Washington-Arlington-Alexandria, DC-VA-MD-WV metropolitan statistical area, classified by FHA as a high-cost area. For 2026, the FHA limits for this metro are:

| Property Type | 2026 FHA Loan Limit (DC Metro) | Typical Use |

|---|---|---|

| 1-Unit (Single-Family) | $1,149,825 | Detached home, townhome, condo |

| 2-Unit (Duplex) | $1,472,250 | Live in one, rent the other |

| 3-Unit (Triplex) | $1,779,525 | Owner-occupied house hack |

| 4-Unit (Fourplex) | $2,211,600 | Maximum FHA multi-unit financing |

For perspective, the national FHA "floor" for low-cost areas in 2026 is roughly $524,225 for a single-family home. Northern Virginia's limit is more than double that — a direct reflection of the region's home values. This is one of the areas where national sites like Bankrate or NerdWallet often show the wrong number, because they default to the national figure rather than the DC metro high-cost limit.

Free · No Commitment

See Exactly What You Qualify For

Get pre-approved in minutes and find out your real FHA buying power in the Northern Virginia market. No cost, no obligation.

Ken Byrne NMLS #187129 · ALCOVA Mortgage LLC NMLS #40508

FHA Limits by Northern Virginia County

A common point of confusion: buyers assume each Northern Virginia county has its own FHA limit. It doesn't. FHA sets limits by metropolitan area, not by individual county, and every Northern Virginia jurisdiction is part of the same Washington-Arlington-Alexandria metro. That means the 1-unit limit is identical across the entire region.

| Jurisdiction | 1-Unit FHA Limit | 4-Unit FHA Limit |

|---|---|---|

| Fairfax County | $1,149,825 | $2,211,600 |

| Loudoun County | $1,149,825 | $2,211,600 |

| Prince William County | $1,149,825 | $2,211,600 |

| Arlington County | $1,149,825 | $2,211,600 |

| City of Alexandria | $1,149,825 | $2,211,600 |

| Falls Church, Fairfax City, Manassas | $1,149,825 | $2,211,600 |

The practical takeaway: wherever you're shopping in Northern Virginia, the FHA number is the same. Your borrowing power doesn't change between Reston and Woodbridge — what changes is local home prices and how far that fixed limit stretches.

How FHA Loan Limits Are Calculated

FHA limits aren't set arbitrarily. They follow a formula tied to the conforming loan limit and local median home prices:

The floor: In low-cost areas, the FHA limit is 65% of the national conforming loan limit (about $524,225 for a single-family home in 2026).

The ceiling: In high-cost areas like the DC metro, the limit rises with local median prices up to a maximum of 150% of the national conforming limit.

Northern Virginia: Because median home values here are well above the national average, the metro is capped at the high-cost ceiling — $1,149,825 for a single-family home in 2026.

Because the calculation is tied to median prices, FHA limits in the DC metro have generally risen year over year as the region's housing market has appreciated. If you saw a lower figure on an older article or a national calculator, it's likely outdated — always confirm the current-year number with a local lender.

FHA vs. Conforming vs. Jumbo in NOVA

The FHA limit is only one of three numbers that matter at Northern Virginia's higher price points. Here's how the three financing tiers compare in the DC metro for 2026:

| Loan Type | Min. Down | Min. Credit | Limit (DC Metro, 1-Unit) | Best For |

|---|---|---|---|---|

| FHA | 3.5% | 580 | $1,149,825 | Lower credit, low down payment |

| Conforming (High-Balance) | 3–5% | 620 | $1,249,125 | Good credit, avoid lifetime MIP |

| Jumbo | 10–20% | 700+ | Above $1,249,125 | High-priced NOVA homes |

Notice that the conforming high-cost limit ($1,249,125) is actually higher than the FHA limit ($1,149,825). So at the very top of FHA's range, a high-balance conventional loan may be the only insured-conforming option. Above $1,249,125, you're in jumbo territory, which requires stronger credit and a larger down payment but has no government insurance cost. Which one is right depends less on the home price and more on your credit profile, down payment, and how long you plan to keep the loan.

Down Payment & Credit Requirements

The headline appeal of an FHA loan is accessibility. Here's what FHA actually requires in 2026:

Minimum Down Payment by Credit Score

On a $600,000 Northern Virginia home, 3.5% down is $21,000 — versus $120,000 for a 20% conventional down payment. That gap is exactly why FHA remains a workhorse loan for first-time buyers in this market. Down payment funds can also come from a gift from family, which is permitted under FHA rules with proper documentation.

Mortgage Insurance: The Trade-Off

Every FHA loan carries mortgage insurance, regardless of down payment. There's an upfront premium (financed into the loan) plus an annual premium paid monthly. On most FHA loans with the minimum down payment, this annual premium stays for the life of the loan. Many borrowers eventually refinance into a conventional loan once they have enough equity to drop mortgage insurance — a strategy worth planning for from day one.

Debt-to-Income Flexibility

FHA's more forgiving debt-to-income tolerance is one reason it works well for buyers carrying student loans or a car payment — common in the DMV's high-cost-of-living environment.

Run the Numbers

What Will Your FHA Payment Be?

Estimate your monthly payment, including mortgage insurance, for any home price in Northern Virginia.

Who Should Use an FHA Loan in Northern Virginia

| FHA Is a Strong Fit If… | Consider Conventional Instead If… |

|---|---|

| Your credit score is in the 580–660 range | Your credit score is 720+ |

| You have limited savings for a down payment | You can put down 10–20% |

| You carry student loans or a higher DTI | You want to avoid lifetime mortgage insurance |

| You're house-hacking a 2–4 unit owner-occupied property | Your target home exceeds $1,149,825 |

There's no universal "best" loan — the right answer depends on your numbers. A good local lender will run both FHA and conventional scenarios side by side so you can see the real monthly and lifetime cost difference before you commit.

How to Get an FHA Loan in Northern Virginia

Check your credit. Pull your score and clean up any errors. At 580+ you unlock the 3.5% down option.

Get pre-approved. A lender verifies income, assets, and credit and issues a pre-approval letter — essential before you make offers in NOVA's competitive market.

Find a home within the limit. Confirm the price keeps your loan amount at or below $1,149,825 (1-unit) for FHA financing.

Complete the FHA appraisal. FHA requires an appraisal that also checks the property meets minimum health and safety standards.

Close. Underwriting finalizes, you sign, and the home is yours — typically 30–45 days from contract.

Ready to Start Your Search?

Browse Homes for Sale in Northern Virginia

Once you know your FHA budget, explore available homes across Loudoun, Fairfax, Prince William, Arlington, and Alexandria.

Common FHA Mistakes to Avoid

- Using the national FHA figure. Plenty of online tools show ~$524,000 — that's the floor, not the DC metro limit. The NOVA number is $1,149,825.

- Assuming county-by-county differences. Every NOVA jurisdiction shares the same metro limit.

- Ignoring lifetime mortgage insurance. With minimum down, the annual premium typically doesn't fall off — plan a refinance exit if equity allows.

- Skipping the conventional comparison. With strong credit, a high-balance conventional loan can be cheaper over time.

- Overlooking the property condition rule. FHA appraisals flag health and safety issues; some fixer-uppers won't pass without repairs first.

- Waiting to get pre-approved. In NOVA's fast market, sellers expect a pre-approval letter with every offer.

If you're buying and selling at the same time — moving up within Northern Virginia, for example — the equity from your current home can fund a larger down payment and help you avoid FHA's mortgage insurance entirely on the next purchase. Coordinating the sale efficiently matters, and a lower listing commission keeps more of that equity working for you.

Buying & Selling?

Keep More of Your Equity With a 1.5% Listing Fee

If you're selling a Northern Virginia home to fund your next purchase, a full-service 1.5% listing program preserves more of the equity you'll roll into your down payment.

The Bottom Line for NOVA Buyers

For 2026, Northern Virginia FHA buyers work with a single-family limit of $1,149,825 across every county and city in the region — one of the highest FHA ceilings in the country. That puts a wide range of NOVA homes within reach with just 3.5% down and a 580 credit score. At the top of the market, a high-balance conventional or jumbo loan takes over, and the right choice between them comes down to your credit, your down payment, and your timeline.

The smartest next step is simple: get pre-approved so you know your exact FHA buying power before you fall in love with a listing. From there, a side-by-side FHA-vs-conventional comparison from a local lender will show you the true cost of each path.

Free · No Commitment

Find Out Your FHA Buying Power Today

Get pre-approved in minutes and see exactly how much home you can buy in Northern Virginia. No cost, no obligation.

Ken Byrne NMLS #187129 · ALCOVA Mortgage LLC NMLS #40508

Frequently Asked Questions

What is the FHA loan limit in Northern Virginia for 2026?

The 2026 FHA loan limit for a single-family (1-unit) home anywhere in Northern Virginia is $1,149,825. The region is part of the high-cost Washington-Arlington-Alexandria metro area, so this limit applies uniformly across all NOVA counties and cities.

Is the FHA limit different in Fairfax County vs. Loudoun County?

No. FHA sets limits by metropolitan area, not by county. Fairfax, Loudoun, Prince William, Arlington, Alexandria, and the rest of Northern Virginia all share the same $1,149,825 single-family limit because they're in the same DC metro.

What credit score do I need for an FHA loan in Virginia?

A 580 FICO qualifies you for the 3.5% minimum down payment. Scores between 500 and 579 require 10% down. Below 500, you're not eligible for FHA financing. Individual lenders may set their own minimums above the FHA floor.

How much down payment do I need for an FHA loan in Northern Virginia?

As little as 3.5% with a 580+ credit score. On a $600,000 NOVA home that's about $21,000. Down payment funds can come from savings or a documented gift from a family member.

What are the FHA multi-unit loan limits in the DC metro for 2026?

For 2026: $1,472,250 for a 2-unit, $1,779,525 for a 3-unit, and $2,211,600 for a 4-unit property. These apply to owner-occupied properties — a popular house-hacking strategy in NOVA.

Can I buy a home priced above the FHA limit?

Yes — but FHA will only insure up to the limit. You'd either bring a larger down payment to keep the loan at or below $1,149,825, or use a high-balance conventional loan (up to $1,249,125) or a jumbo loan for higher price points.

What is the difference between the FHA limit and the conforming loan limit?

In the DC metro for 2026, the FHA single-family limit is $1,149,825 while the conforming high-cost limit is $1,249,125. FHA loans have easier credit and down payment requirements; conforming conventional loans can avoid lifetime mortgage insurance with enough equity.

Does an FHA loan always require mortgage insurance?

Yes. Every FHA loan has an upfront premium plus an annual premium paid monthly. On loans with the minimum down payment, the annual premium generally remains for the life of the loan, which is why many borrowers refinance to conventional once they have enough equity.

What are the closing costs for an FHA loan in Virginia?

Expect roughly 2–5% of the loan amount, including lender fees, title insurance, the appraisal, and Virginia-specific costs like the grantor tax and recordation/deed of trust tax. The FHA upfront mortgage insurance premium is typically financed into the loan rather than paid at closing.

How do I get pre-approved for an FHA loan in Northern Virginia?

Contact a licensed local lender, provide income, asset, and credit documentation, and the lender will issue a pre-approval letter showing your FHA buying power. You can start an application online with ALCOVA Mortgage and speak directly with Ken Byrne, NMLS #187129.

Is it a good time to buy in Northern Virginia in 2026?

Northern Virginia remains a strong, stable market driven by federal employment, defense, and tech demand. The right time depends on your finances more than market timing — a pre-approval clarifies your true budget so you can act with confidence when the right home appears. Rates vary; current rates are available through your lender.

How do I find a good mortgage lender in Northern Virginia?

Look for a licensed lender with local DMV market experience, transparent fee disclosure, responsive communication, and the ability to run FHA and conventional scenarios side by side. Ken Byrne, NMLS #187129, with ALCOVA Mortgage LLC (NMLS #40508), is licensed in VA, MD, DC, and WV and specializes in the Northern Virginia market.

Glossary

FHA Loan: A mortgage insured by the Federal Housing Administration, designed for buyers with lower credit scores or smaller down payments.

FHA Loan Limit: The maximum loan amount FHA will insure for a property of a given size in a given metro area.

High-Cost Area: A region where median home prices push loan limits above the national baseline, up to a defined ceiling.

Conforming Loan Limit: The maximum loan amount eligible for purchase by Fannie Mae and Freddie Mac, set annually by the FHFA.

Mortgage Insurance Premium (MIP): The insurance cost on an FHA loan — an upfront premium plus an annual premium paid monthly.

Jumbo Loan: A mortgage that exceeds the conforming loan limit, requiring stronger credit and a larger down payment.

Debt-to-Income Ratio (DTI): The percentage of your gross monthly income that goes toward debt payments — a key qualification metric.

Pre-Approval: A lender's conditional commitment to lend a specific amount based on verified income, assets, and credit.

Disclaimer: This article is for informational purposes only and does not constitute financial or legal advice. Mortgage programs, rates, and eligibility requirements are subject to change. Contact a licensed mortgage professional for guidance specific to your situation. Ken Byrne, NMLS #187129 · ALCOVA Mortgage LLC, NMLS #40508 · Licensed in VA, MD, DC, WV.

Categories

Recent Posts

GET MORE INFORMATION

Broker Associate