How Much Is a Mortgage on a $500,000 House? Full Payment Breakdown

How Much Is a Mortgage on a $500,000 House? Full Payment Breakdown

A $500,000 house is right in the sweet spot for the DMV market — common in outer Loudoun, Prince William, Frederick County (MD), Stafford, and parts of Fairfax. But the sticker price is only the start of the story. Your actual monthly payment depends on your down payment, loan type, property taxes, insurance, mortgage insurance, and HOA dues. Two buyers with the same $500,000 home can end up with monthly payments that differ by more than $1,000.

This guide breaks down exactly what a mortgage on a $500,000 house costs in 2026 — every line item, every loan type, and every down payment scenario — so you can budget with confidence before you make an offer.

Quick Answer: A mortgage on a $500,000 house typically runs $3,300–$4,200 per month in the DMV when you include principal, interest, property taxes, homeowners insurance, and mortgage insurance. With 20% down ($100,000), you can expect roughly $3,400/month total. With 5% down on a conventional loan, total payment runs closer to $4,000/month including PMI. To comfortably afford a $500,000 home, most buyers need a household income of $125,000–$155,000 depending on debt and down payment.

Key Takeaways

- Principal & interest on a $500,000 home with 20% down is roughly $2,660/month at a 7% rate; with 5% down it rises to about $3,160/month.

- Property taxes in Northern Virginia add roughly $435–$485/month; Maryland counties run $400–$500/month; DC adds $355/month at the standard rate.

- Homeowners insurance averages $120–$180/month for a $500,000 home in the DMV.

- PMI or MIP can add $150–$340/month if your down payment is below 20%.

- VA and USDA loans require 0% down, eliminating PMI entirely (though VA has a one-time funding fee).

- Closing costs in Virginia typically run $10,000–$18,000 on a $500,000 purchase, with the recordation tax being a notable Virginia-specific line item.

Table of Contents

- The Five Parts of a Mortgage Payment (PITI + HOA)

- Payment by Down Payment: 3%, 5%, 10%, 20%

- Payment by Loan Type: Conventional, FHA, VA, USDA

- What Income Do You Need to Afford a $500,000 House?

- Closing Costs on a $500,000 Home in VA, MD, and DC

- Property Taxes by DMV County

- How Interest Rates Change Your Payment

- Total Cost Over 30 Years

- 7 Ways to Lower Your $500,000 Mortgage Payment

- Frequently Asked Questions

- Glossary of Mortgage Terms

The Five Parts of a Mortgage Payment (PITI + HOA)

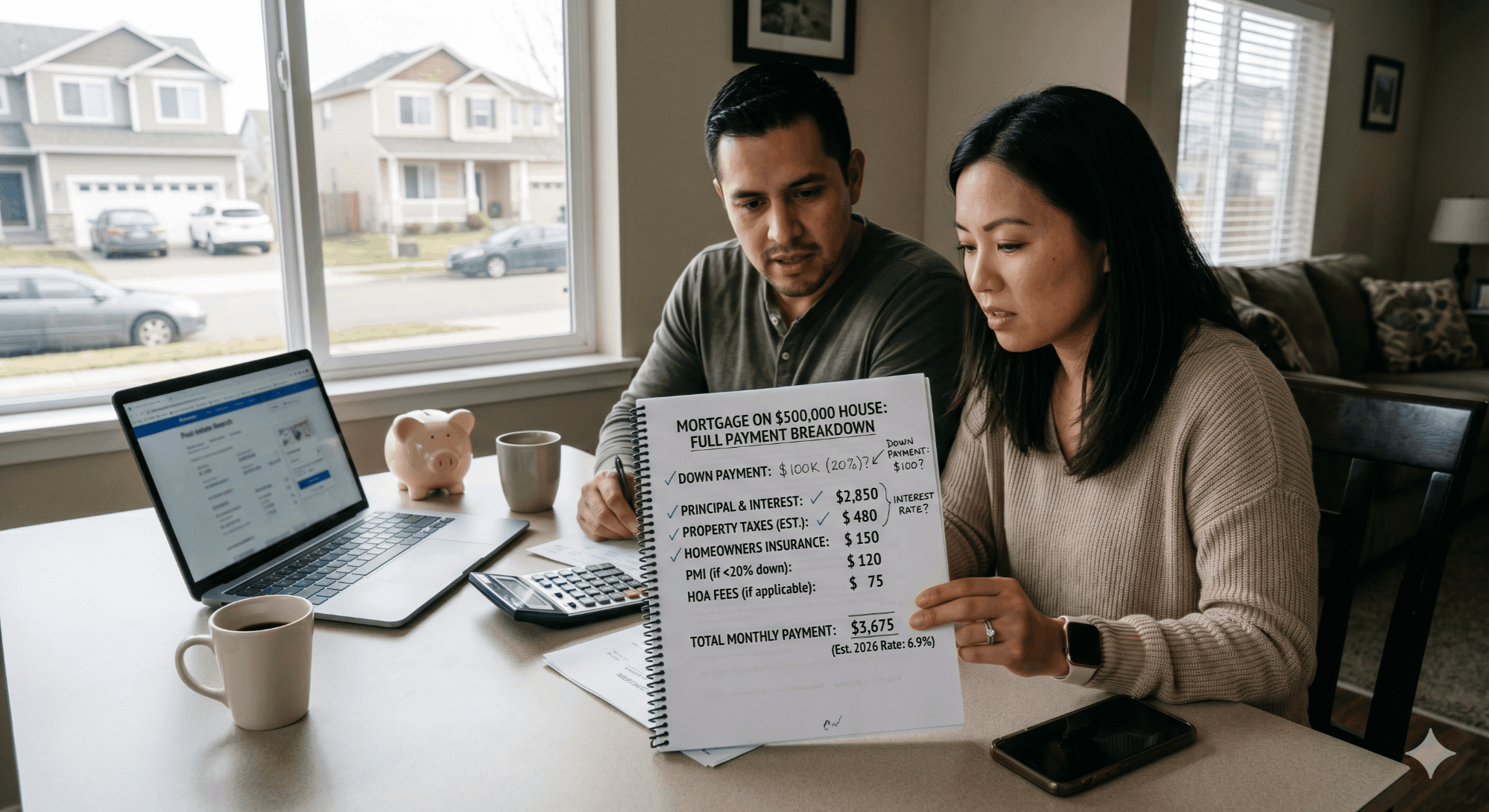

Most homebuyers focus on the principal and interest figure their lender quotes — but that's only part of what you'll actually pay each month. Your full housing payment is known as PITI: Principal, Interest, Taxes, and Insurance — plus HOA dues and mortgage insurance when applicable. Here's what each component looks like for a $500,000 house.

1. Principal & Interest (P&I)

This is the portion of your payment that pays down the loan and the cost of borrowing. It's set by your loan amount, interest rate, and loan term (typically 30 years). On a $400,000 loan (a $500,000 home with 20% down) at a hypothetical 7% rate, P&I works out to roughly $2,661 per month. Your actual rate will vary — current rates are available through your lender.

2. Property Taxes (T)

Your county assesses property taxes annually based on your home's assessed value. The lender collects this monthly via escrow and pays it on your behalf. For a $500,000 home, expect roughly $4,250–$5,950/year in DMV jurisdictions, or about $355–$495 per month.

3. Homeowners Insurance (I)

Your lender requires you to carry a homeowners insurance policy that covers the dwelling. For a $500,000 home in the DMV, average premiums run $1,400–$2,200/year — about $120–$180/month — depending on the home's age, construction, and location.

4. Mortgage Insurance (PMI or MIP)

If your down payment is below 20% on a conventional loan, you'll pay private mortgage insurance (PMI). On an FHA loan, you'll pay mortgage insurance premium (MIP) regardless of down payment. PMI on a $500,000 home with 5% down typically runs $180–$280/month and drops off automatically once you reach 22% equity. FHA MIP runs about $300–$340/month and lasts the life of the loan unless you refinance into a conventional loan.

5. HOA Dues

If you're buying in an HOA community — common in NOVA neighborhoods like Brambleton, Broadlands, Reston, Stone Ridge, and Lansdowne — HOA dues are paid directly to the association, not the lender. They typically range from $80 to $400/month for single-family homes and $250–$600/month for townhomes and condos. While not part of your mortgage payment, lenders count HOA dues against your debt-to-income (DTI) ratio when qualifying you, so they directly affect what you can afford.

Free · No Commitment

See What You Qualify For Today

Get pre-approved in minutes and know exactly how much home you can afford in the DC metro market. No cost, no obligation.

Ken Byrne NMLS #187129 · ALCOVA Mortgage LLC NMLS #40508

Payment by Down Payment: 3%, 5%, 10%, 20%

Your down payment is the single biggest lever in your monthly mortgage payment. Below is a side-by-side comparison of total monthly payments at four different down payment levels for a $500,000 home, using a hypothetical 7% interest rate (rates vary; this is illustrative only). Property tax is estimated using the Loudoun County rate (~1.045%), and PMI estimates assume average 740 credit.

| Down Payment | Loan Amount | P&I | Tax + Ins. | PMI | Total Monthly |

|---|---|---|---|---|---|

| 3% ($15,000) | $485,000 | $3,227 | $585 | $280 | $4,092 |

| 5% ($25,000) | $475,000 | $3,161 | $585 | $220 | $3,966 |

| 10% ($50,000) | $450,000 | $2,994 | $585 | $155 | $3,734 |

| 20% ($100,000) | $400,000 | $2,661 | $585 | $0 | $3,246 |

Illustrative figures only. Actual payments vary by rate, credit profile, and county tax rate. Rates change daily — your actual rate will be quoted at application.

Visual: Monthly Payment by Down Payment

The takeaway: increasing your down payment from 5% to 20% saves about $720 per month — most of that from eliminating PMI and lowering the loan balance. Over 30 years, that's more than $250,000 in savings, before even accounting for interest reduction.

Payment by Loan Type: Conventional, FHA, VA, USDA

A $500,000 home is fully within the conforming loan limit in every DMV market — the 2026 high-cost limit for the DC metro is $1,249,125 for a single-family conforming loan, and the FHA limit is $1,149,825. That means you have access to every major loan type. Here's how each one stacks up.

| Loan Type | Min. Down | Min. Credit | Mortgage Ins. | Best For |

|---|---|---|---|---|

| Conventional | 3% | 620 | PMI (drops off) | Strong credit, planning equity |

| FHA | 3.5% | 580 | MIP (life of loan) | Lower credit scores |

| VA | 0% | ~620 | None (funding fee) | Veterans, active-duty, surviving spouses |

| USDA | 0% | 640 | Annual fee | Outer NOVA, rural Loudoun & Prince William |

Conventional Loan: 5% Down on a $500,000 Home

A conventional loan with 5% down is the most common scenario for first-time and move-up buyers without veteran benefits. You'll need $25,000 plus closing costs at the table, and PMI will add roughly $180–$280/month — but it drops off automatically once your loan balance reaches 78% of the original purchase price (typically year 8–11). For buyers with strong credit (740+) who don't have a VA benefit, this is usually the best loan.

FHA Loan: 3.5% Down on a $500,000 Home

FHA is designed for buyers with credit between 580 and 700 or those who want a lower down payment. You'll need $17,500 down. The catch: FHA's mortgage insurance premium (MIP) is paid for the life of the loan unless you refinance, and runs roughly $300–$340/month on a $482,500 loan. Many borrowers use FHA to get into a home, then refinance to conventional once they hit 20% equity.

VA Loan: 0% Down on a $500,000 Home

If you're a veteran, active-duty service member, or qualifying surviving spouse, the VA loan is almost always the best option for a $500,000 home in the DMV. No down payment, no monthly mortgage insurance, and competitive rates. There is a one-time VA funding fee (typically 2.15% for first-time use, financeable into the loan), but disabled veterans are exempt. Northern Virginia's enormous military population — Pentagon, Fort Belvoir, Quantico, Joint Base Andrews — makes this the dominant loan type for many of our buyers.

USDA Loan: 0% Down in Eligible Areas

USDA loans are 0% down with reduced mortgage insurance, but they're geographically restricted to USDA-eligible "rural" areas. In the DMV, that includes parts of western Loudoun, much of rural Prince William, large portions of Fauquier, Spotsylvania, Stafford (outside the city), and most of the Eastern Shore. There are also income limits — typically around $130,000–$155,000 for a 1–4 person household in NOVA, depending on county. A $500,000 home is within USDA's purchase price range in most eligible markets.

Run the Numbers

What Will Your Monthly Payment Be?

Use our mortgage calculator to estimate your monthly payment for any home price in Virginia, Maryland, or DC.

What Income Do You Need to Afford a $500,000 House?

Lenders qualify you using debt-to-income ratio (DTI) — the percentage of your gross monthly income that goes toward your housing payment plus all other debts. The two most common DTI thresholds:

- Front-end DTI — your housing payment alone — capped at roughly 28%–31%

- Back-end DTI — housing plus all other debts (car loans, student loans, credit cards) — capped at 43%–50% depending on the loan program

For a $500,000 home with a $3,966 monthly payment (5% down conventional scenario), here's the income required at different DTI levels:

| Other Monthly Debt | Total Debt + Housing | Min. Income (43% DTI) | Comfortable (36% DTI) |

|---|---|---|---|

| $0 | $3,966 | $110,700/yr | $132,200/yr |

| $500 (1 car) | $4,466 | $124,650/yr | $148,900/yr |

| $900 (car + student loan) | $4,866 | $135,800/yr | $162,200/yr |

| $1,500 (multiple debts) | $5,466 | $152,500/yr | $182,200/yr |

Most DMV lenders will approve borrowers up to 45%–50% DTI on conventional and 50%–57% on FHA, but just because you can qualify doesn't mean you should. The 36% benchmark is a healthier long-term target — leaving room for retirement savings, emergencies, and lifestyle.

Closing Costs on a $500,000 Home in VA, MD, and DC

Closing costs in the DMV typically run 2%–4% of the purchase price for the buyer — that's $10,000–$20,000 on a $500,000 home — before lender credits, seller concessions, or down payment assistance. The mix differs by jurisdiction.

Virginia Closing Cost Breakdown ($500,000 Purchase, 5% Down)

| Cost Item | Estimate | Notes |

|---|---|---|

| Lender fees (origination, underwriting, processing) | $1,500–$2,800 | Varies by lender |

| Appraisal | $650–$850 | Required by lender |

| Title insurance (owner's + lender's) | $2,200–$3,500 | Owner's policy is optional but recommended |

| Recordation tax (VA state + locality) | ~$1,800 | $0.25 per $100 of loan + state portion |

| Prepaid taxes & insurance (escrow setup) | $3,500–$5,500 | ~6 months of taxes + 12 months insurance |

| Settlement / attorney fees | $700–$1,200 | Title company or attorney |

| Home inspection | $450–$650 | Usually paid before closing |

| Total Buyer Closing Costs | $10,800–$15,300 | Plus down payment |

In Maryland, the recordation tax is higher (typically 0.5%–1.5% combined state and county), and there's also a transfer tax. In DC, the buyer pays a recordation tax of 1.1%–1.45% depending on price, and there's also a deed transfer tax — bringing total closing costs noticeably higher than Virginia for the same purchase price.

Property Taxes by DMV County (on a $500,000 Home)

Property tax rates vary significantly across the DMV. On a $500,000 assessed value, here's what your annual and monthly tax bill looks like in each major jurisdiction (2026 rates):

| Jurisdiction | Effective Rate | Annual Tax | Monthly |

|---|---|---|---|

| Arlington County, VA | ~1.013% | $5,065 | $422 |

| Loudoun County, VA | ~1.045% | $5,225 | $435 |

| Fairfax County, VA | ~1.135% | $5,675 | $473 |

| Prince William County, VA | ~1.085% | $5,425 | $452 |

| Montgomery County, MD | ~0.987% | $4,935 | $411 |

| Frederick County, MD | ~1.060% | $5,300 | $442 |

| Washington, DC | ~0.85% | $4,250 | $354 |

DC's lower rate is partially offset by the homestead deduction available to owner-occupants, but DC also charges a recordation tax at closing that exceeds Virginia's. Maryland's rates appear moderate, but Maryland buyers also face a state transfer tax and county-specific recordation taxes that add to closing costs.

Free · No Commitment

Get a Custom Payment Estimate for Your County

A pre-approval includes a precise monthly payment based on your credit, down payment, and the exact county you're shopping in.

Ken Byrne NMLS #187129 · ALCOVA Mortgage LLC NMLS #40508

How Interest Rates Change Your Payment

Rates move daily and can shift the principal-and-interest portion of your payment by hundreds of dollars per month. Here's how a $400,000 loan (the financed amount on a $500,000 home with 20% down) plays out at different rate environments. These are illustrative — your actual rate will be quoted at application based on your credit profile, loan type, and current market conditions.

| Rate | Monthly P&I | Lifetime Interest | vs. 7% |

|---|---|---|---|

| 5.5% | $2,271 | $417,560 | −$390/mo |

| 6.0% | $2,398 | $463,360 | −$263/mo |

| 6.5% | $2,528 | $510,180 | −$133/mo |

| 7.0% | $2,661 | $558,030 | baseline |

| 7.5% | $2,797 | $606,890 | +$136/mo |

A 1.5-percentage-point rate difference (5.5% vs. 7.0%) changes your monthly payment by nearly $400 — and changes your total interest paid by more than $140,000 over 30 years. This is why locking your rate at the right time and shopping multiple lenders matters.

Total Cost Over 30 Years

A $500,000 home isn't a $500,000 expense. Over a 30-year mortgage at 7%, the total cost looks dramatically different depending on your down payment.

Most homeowners don't keep the same loan for 30 years — average mortgage life is 7–9 years before refinancing or selling — so these numbers are illustrative. But the gap between scenarios is real, and the case for refinancing FHA into conventional once you reach 20% equity is straightforward arithmetic.

7 Ways to Lower Your $500,000 Mortgage Payment

- Increase your down payment. Going from 5% to 20% saves PMI plus reduces the loan balance — over $700/month in our scenario.

- Improve your credit score before applying. Moving from 680 to 740+ can drop your rate meaningfully and reduce PMI cost.

- Buy down your rate with discount points. One point (1% of the loan) typically lowers your rate by 0.25%. On a $475,000 loan that's $4,750 upfront for ~$80/month savings.

- Use a VA loan if you're eligible. Zero down, no monthly mortgage insurance, often the lowest rate.

- Use down payment assistance. Virginia Housing's DPA Grant, the Maryland Mortgage Program, or DC's HPAP (up to $202,000 in DC) can dramatically reduce your cash to close.

- Negotiate seller concessions. In a balanced market, sellers often agree to pay 2%–3% of closing costs, freeing your cash for down payment.

- Choose the right loan term. A 15-year mortgage saves enormous interest, but doubles your monthly payment. A 30-year keeps payment manageable for budget-conscious buyers.

Ready to Start Your Search?

Browse $500,000 Homes in Northern Virginia

Once you know your budget, explore available homes across Loudoun, Fairfax, Prince William, Arlington, and Alexandria.

Frequently Asked Questions

How much is a mortgage on a $500,000 house?

A mortgage on a $500,000 house in the DMV typically runs $3,300–$4,200 per month including principal, interest, property taxes, homeowners insurance, and mortgage insurance. With 20% down ($100,000), expect roughly $3,400/month total. With 5% down on a conventional loan, expect about $4,000/month.

What income do I need to afford a $500,000 house in Northern Virginia?

Most buyers need a household income of $125,000–$155,000 to comfortably afford a $500,000 home in Northern Virginia, depending on their down payment and other monthly debts. Lenders may technically approve you up to 50% DTI, but a 36% back-end DTI keeps your finances healthier long-term.

What credit score do I need for a $500,000 mortgage in Virginia?

580 for FHA, 620 for conventional and VA, 640 for USDA. Higher scores qualify for lower rates and lower PMI. Borrowers with 740+ generally see the best pricing on conventional loans.

How much down payment do I need for a $500,000 house?

As little as 0% with a VA or USDA loan, 3% with a conventional first-time buyer program, 3.5% with FHA, or 5% with standard conventional. 20% ($100,000) eliminates PMI on a conventional loan and produces the lowest monthly payment.

What are the closing costs on a $500,000 house in Virginia?

Closing costs in Virginia typically run 2%–4% of the purchase price for the buyer — about $10,000–$20,000 on a $500,000 home. The Virginia recordation tax (~$0.25 per $100 of loan amount, plus state portion), title insurance, lender fees, prepaid taxes and insurance, and the appraisal are the largest line items.

What is the conforming loan limit in the DC metro for 2026?

The 2026 conforming loan limit in the DC metro (a high-cost area) is $1,249,125 for a single-family home. The FHA loan limit is $1,149,825. A $500,000 loan is well within both limits, so you have full access to conforming and FHA financing.

How much is PMI on a $500,000 house?

PMI on a conventional $500,000 home with 5% down typically runs $180–$280/month for borrowers with 720+ credit. It drops off automatically when your loan balance reaches 78% of the original purchase price. FHA's mortgage insurance (MIP) runs about $300–$340/month and lasts the life of the loan unless you refinance.

Is it cheaper to buy a $500,000 house in Maryland or Virginia?

Property tax rates are similar in both states (around 1% effective), but closing costs in Virginia tend to be lower than Maryland because Maryland has higher transfer and recordation taxes. DC has the lowest property tax rate of the three but the highest closing-cost recordation taxes. Total cost depends on jurisdiction, not just state.

Can I get a $500,000 mortgage with no down payment?

Yes — if you qualify for a VA loan (veteran, active-duty, or surviving spouse) or a USDA loan (in eligible rural areas, with income limits). Both loan types finance 100% of the purchase price. Down payment assistance programs like Virginia Housing DPA Grant and DC HPAP can also reduce or eliminate your down payment with conventional or FHA loans.

Should I buy a $500,000 house with 5% down or wait for 20%?

Depends on your timeline and the market. Putting 20% down saves PMI and reduces your payment by hundreds per month — but the time it takes to save another $75,000 in the DMV is often two to four years, during which home prices and rents typically rise. For many buyers, buying at 5% down sooner and refinancing or paying down to 20% equity over time is the better long-term math. Run both scenarios with a lender before deciding.

How do I find a good mortgage lender in Northern Virginia?

Look for a licensed loan officer (verifiable at nmlsconsumeraccess.org), strong DMV market knowledge, responsive communication, a full slate of loan programs (Conventional, FHA, VA, USDA, jumbo, Virginia Housing), and transparent fees disclosed in a Loan Estimate. Ken Byrne (NMLS #187129) at ALCOVA Mortgage LLC (NMLS #40508) operates JB Financing and serves buyers across Virginia, Maryland, DC, and West Virginia.

Is now a good time to buy a $500,000 house in the DMV?

Inventory in 2026 has improved versus the 2021–2023 lows, giving buyers more leverage on negotiation and contingencies. Rates remain elevated versus the historic lows of 2020–2021 but have stabilized. The decision is personal — based on your income stability, savings, life timeline, and how long you plan to stay in the home. A 5+ year time horizon makes buying compelling at almost any market point in the DMV.

Glossary of Mortgage Terms

PITI — Principal, Interest, Taxes, and Insurance. The four components of a typical mortgage payment.

PMI (Private Mortgage Insurance) — Insurance required on conventional loans with less than 20% down. Drops off automatically at 78% LTV.

MIP (Mortgage Insurance Premium) — FHA's version of mortgage insurance. Required regardless of down payment. Lasts the life of the loan unless you refinance.

DTI (Debt-to-Income Ratio) — Your monthly debts divided by gross monthly income. Front-end DTI is housing only; back-end DTI includes all debts.

LTV (Loan-to-Value) — Loan amount divided by home value. 80% LTV = 20% down. PMI drops off at 78% LTV.

Escrow — An account managed by your lender that collects monthly portions of your property taxes and insurance, then pays them when due.

Conforming Loan Limit — The maximum loan size eligible for purchase by Fannie Mae and Freddie Mac. The 2026 high-cost limit in the DC metro is $1,249,125 for a single-family home.

Discount Points — Optional upfront fees paid to lower your interest rate. One point (1% of loan) typically reduces the rate by 0.25%.

Next Steps: Make the Numbers Real for Your Situation

The figures in this guide are realistic illustrations — but your actual payment depends on your credit, down payment, loan type, and the specific county you're buying in. The fastest way to get a real, customized monthly payment estimate is to start a pre-approval. It takes minutes, doesn't cost anything, and gives you a Loan Estimate with exact figures you can budget around.

JB Financing is the mortgage lending operation of Ken Byrne (NMLS #187129), Branch Partner at ALCOVA Mortgage LLC (NMLS #40508). ALCOVA is licensed in Virginia, Maryland, DC, and West Virginia and offers Conventional, FHA, VA, USDA, jumbo, and Virginia Housing programs. Direct contact: kbyrne@alcova.com or (703) 927-4456.

Free · No Commitment

Get Your Exact $500,000 Payment Estimate

Start your pre-approval to get a precise monthly payment based on your credit, down payment, and target county.

Ken Byrne NMLS #187129 · ALCOVA Mortgage LLC NMLS #40508

Disclaimer: This article is for informational purposes only and does not constitute financial or legal advice. Mortgage programs, rates, and eligibility requirements are subject to change. Sample payment figures use illustrative interest rates for comparison only and are not rate quotes. Contact a licensed mortgage professional for guidance specific to your situation. Ken Byrne, NMLS #187129 · ALCOVA Mortgage LLC, NMLS #40508 · Licensed in VA, MD, DC, WV.

Categories

Recent Posts

GET MORE INFORMATION

Broker Associate