Mortgage Pre-Approval in Northern Virginia: Step-by-Step Guide

Mortgage Pre-Approval in Northern Virginia: Step-by-Step Guide

By Ken Byrne, NMLS #187129 · ALCOVA Mortgage LLC, NMLS #40508 · Updated for 2026

Quick Answer: Mortgage pre-approval in Northern Virginia is a verified review of your income, credit, assets, and debts that confirms how much a lender will let you borrow. The process typically takes 1–3 business days once you submit complete documentation, your pre-approval letter is usually valid for 60–90 days, and most NoVA sellers will not accept an offer without one. To get pre-approved, you'll submit pay stubs, W-2s/tax returns, bank statements, and authorize a credit pull — and a licensed loan officer will issue a written letter stating your maximum loan amount.

Key Takeaways

- Pre-approval is not prequalification. Prequalification is a soft estimate; pre-approval is a verified credit decision based on documented income, assets, and a hard credit pull.

- In NoVA, pre-approval is essentially required. Listing agents in Fairfax, Loudoun, Arlington, and Prince William routinely reject offers that don't include a current pre-approval letter from a licensed lender.

- 2026 conforming loan limit (DC metro): $1,249,125 for single-family — meaning many NoVA buyers can stay in conforming territory even on higher-priced homes.

- Most lenders require a minimum credit score of 620 for conventional loans and 580 for FHA, though stronger scores unlock better pricing.

- Pre-approval letters typically last 60–90 days, after which you'll need updated documents to reissue.

- Don't open new credit, change jobs, or move large sums between pre-approval and closing — any of those can derail your loan.

Table of Contents

- What Is Mortgage Pre-Approval?

- Pre-Approval vs. Prequalification vs. Underwritten Approval

- Why Pre-Approval Matters So Much in Northern Virginia

- The Step-by-Step Pre-Approval Process

- Documents You'll Need

- Credit Score and DTI Requirements

- How Long Pre-Approval Takes (and Lasts)

- What's Inside a Pre-Approval Letter

- Common Mistakes That Derail Pre-Approval

- What Happens After You're Pre-Approved

- Frequently Asked Questions

- Mortgage Glossary

If you're planning to buy a home in Fairfax, Loudoun, Arlington, Prince William, or Alexandria, getting mortgage pre-approval is the first real step — not the last. In a competitive market like Northern Virginia, where well-priced homes still attract multiple offers and listing agents screen buyers carefully, an offer without a pre-approval letter is rarely taken seriously.

But "pre-approval" is one of the most misunderstood terms in real estate. It's not the same as prequalification, it's not a guarantee of final loan approval, and the quality of the letter you carry into a negotiation depends entirely on how thoroughly your lender vetted you.

This guide walks through the full pre-approval process step by step — what it is, how it differs from a prequal, what documents you'll need, what credit score actually matters, how long it takes, what's inside the letter, and how to keep your file clean between pre-approval and closing. If you've never bought a home in the DMV before, or it's been long enough that you're due for a refresher, this is the foundation.

What Is Mortgage Pre-Approval?

Mortgage pre-approval is a written commitment from a licensed lender stating the maximum loan amount you qualify for, based on a documented review of your finances. It's not a final loan approval — that comes later, after you have a specific property under contract — but it's the strongest indicator a seller has that you can actually close on a purchase.

During pre-approval, your loan officer will:

- Pull your credit — a hard inquiry that produces a tri-merge report from Equifax, Experian, and TransUnion.

- Verify your income — pay stubs, W-2s, and tax returns for self-employed or commission borrowers.

- Verify your assets — bank statements showing the funds you'll use for down payment, closing costs, and reserves.

- Calculate your debt-to-income ratio (DTI) — your total monthly debts divided by gross monthly income.

- Run automated underwriting — using Fannie Mae's Desktop Underwriter (DU) or Freddie Mac's Loan Product Advisor (LPA) for conventional loans, or the equivalent for FHA, VA, and USDA.

- Issue your pre-approval letter — a one-page document showing your maximum purchase price, loan type, and key conditions.

A real pre-approval is rooted in documentation. If a lender hands you a letter after a 5-minute phone call without ever seeing a pay stub, that's a prequalification — not a pre-approval — no matter what the letter says at the top.

Pre-Approval vs. Prequalification vs. Underwritten Approval

There are three distinct levels of mortgage qualification, and the differences matter a lot once you start writing offers in Northern Virginia.

| Level | Documentation | Credit Pull | Strength of Offer | Best For |

|---|---|---|---|---|

| Prequalification | None — verbal estimates | Optional / soft | Weak | Early budgeting |

| Pre-Approval | Full — pay stubs, W-2s, bank statements | Hard pull | Strong | Active home shopping |

| Underwritten Approval (TBD) | Full + reviewed by underwriter | Hard pull | Strongest | Multiple-offer situations |

An underwritten pre-approval (sometimes called a "TBD approval" — meaning the property is To Be Determined) is the gold standard. Your file has been reviewed not just by a loan officer but by an actual underwriter, with all conditions cleared except those tied to a specific property. In a multiple-offer scenario in Arlington or Loudoun, an underwritten letter can put you ahead of buyers with standard pre-approvals — sometimes even ahead of cash offers — because the seller knows you can close fast.

Why Pre-Approval Matters So Much in Northern Virginia

Northern Virginia's housing market has a few characteristics that make pre-approval more important here than in many other parts of the country:

1. High Median Prices Mean Larger Loans

Median home prices in Fairfax, Loudoun, and Arlington routinely sit in the $700,000–$900,000 range, with $1M+ common in inside-the-Beltway markets. Larger loans mean tighter scrutiny — and a casual prequal isn't going to convince a seller you can actually qualify for a $750,000 mortgage.

2. Listing Agents Pre-Screen Offers

Most experienced NoVA listing agents will call your loan officer before presenting your offer to the seller. They want to know: Did you actually see pay stubs? Was credit pulled? Have you reviewed assets? A loan officer who says "I haven't seen documents yet" is a red flag that often kills the offer before the seller ever sees it.

3. Federal Government and Contractor Income Is Common — and Complex

In NoVA, a huge share of buyers are federal employees, military, defense contractors, or work for companies tied to government contracting. Income structures often include base pay, locality pay, bonuses, special pays (BAH for VA loans), and sometimes RSUs or contracting income. Each of those needs to be documented correctly during pre-approval — and a generic online lender often gets it wrong.

4. The Conforming Loan Limit Is Higher Here

The 2026 conforming loan limit for the DC metro high-cost area is $1,249,125 for a single-family home — substantially higher than the standard national limit. That means many NoVA buyers who would face jumbo financing elsewhere can still qualify for conforming products with better terms — but only if their lender prices and structures the loan correctly during pre-approval.

Free · No Commitment

See What You Qualify For Today

Get pre-approved in minutes and know exactly how much home you can afford in the DC metro market. No cost, no obligation.

Ken Byrne NMLS #187129 · ALCOVA Mortgage LLC NMLS #40508

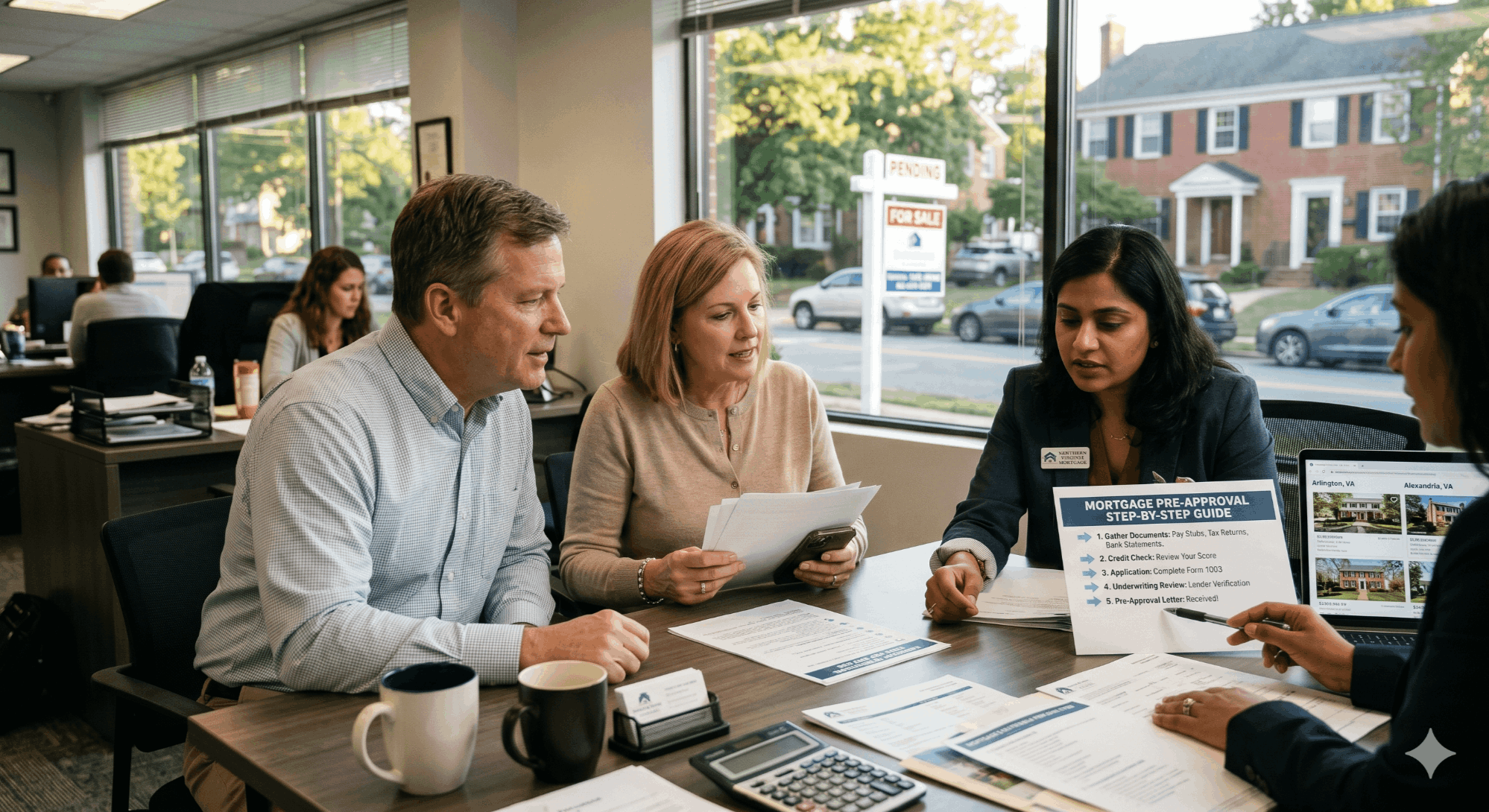

The Step-by-Step Pre-Approval Process

Here's exactly what happens when you apply for mortgage pre-approval in Northern Virginia, from first phone call to letter in hand.

Initial Conversation with a Loan Officer

A 15–30 minute conversation about your goals, target price range, location, employment situation, and whether you've owned a home before. The loan officer will recommend loan programs to consider — conventional, FHA, VA, USDA — and outline what documentation you'll need.

Complete the Loan Application (Form 1003)

You'll fill out the Uniform Residential Loan Application — typically online through your lender's secure portal. It captures personal information, employment, income, assets, debts, and the property type you're targeting.

Authorize a Credit Pull

Your lender will run a tri-merge credit report. The score they use for qualifying is the middle of the three (or the lower of two if you have a co-borrower). Multiple mortgage credit pulls within a 45-day window count as a single inquiry for FICO scoring purposes, so don't be afraid to compare lenders.

Submit Income & Asset Documentation

Upload pay stubs, W-2s, tax returns (if needed), bank statements, and identification. Most lenders use a secure document portal so you don't have to email sensitive PDFs.

Loan Officer Reviews Your File

Your loan officer calculates qualifying income, debt-to-income ratio, and asset reserves. They identify any red flags — gaps in employment, recent large deposits without a paper trail, derogatory credit items — and request additional documentation as needed.

Run Automated Underwriting (DU/LPA)

Your file is run through Fannie Mae's Desktop Underwriter or Freddie Mac's Loan Product Advisor. The system returns an "Approve/Eligible" or "Refer" decision and a list of conditions — items that must be cleared for the file to move forward.

Receive Your Pre-Approval Letter

Your lender issues a written letter showing the maximum loan amount, loan program, estimated rate environment, and any standard contingencies (final property appraisal, title review, etc.). You'll provide this letter with every offer you write.

Optional: Upgrade to Underwritten Pre-Approval

If you're entering a competitive market, ask your lender to send the file to underwriting for a TBD review. This adds 2–5 business days but gives you a substantially stronger letter — particularly valuable for offers in Arlington, McLean, Vienna, or anywhere with multiple-offer situations.

Documents You'll Need

Gather these before you start the application — having everything ready can shave days off your timeline.

Standard Pre-Approval Document Checklist

Income (W-2 Employees)

- Most recent 30 days of pay stubs

- W-2 forms for the past 2 years

- Most recent 2 years of federal tax returns (if you have non-W-2 income, RSUs, or itemize heavily)

Income (Self-Employed / 1099 / Business Owners)

- 2 years of personal tax returns (all schedules)

- 2 years of business tax returns if you own 25%+ of a business

- Year-to-date profit & loss statement

- Most recent 2 months of business bank statements

Assets

- Most recent 2 months of statements for all accounts you'll use for down payment, closing costs, or reserves (checking, savings, money market, brokerage, retirement)

- Documentation of any large deposits in the last 60 days that aren't paychecks

- Gift letter and donor's bank statement if any down payment money is a gift

Identification & Other

- Driver's license or government-issued photo ID

- Social Security number (for credit pull)

- Certificate of Eligibility (COE) for VA loans — your lender can pull this for you

- DD-214 if you're a veteran

- Divorce decree or child support order if applicable

- Bankruptcy discharge papers if you've filed in the past 7 years

Credit Score and DTI Requirements

Two numbers carry the most weight in pre-approval: your credit score and your debt-to-income ratio.

Minimum Credit Scores by Loan Type

| Loan Type | Typical Minimum Score | Best Pricing At | Notes |

|---|---|---|---|

| Conventional | 620 | 740+ | Pricing tiers in 20-point bands |

| FHA | 580 (3.5% down) | 680+ | 500–579 possible with 10% down |

| VA | 580–620 (lender-set) | 700+ | No VA-mandated minimum; varies by lender |

| USDA | 640 | 700+ | Manual underwriting possible below 640 |

Debt-to-Income (DTI) Ratio Limits

Your DTI is your total monthly debt obligations (the new mortgage payment plus all minimum payments on credit cards, car loans, student loans, etc.) divided by your gross monthly income. Most automated underwriting systems are comfortable up to:

In Northern Virginia specifically, where buyers often carry student loan debt and where new homes in master-planned communities like Brambleton, Broadlands, and One Loudoun include HOA fees that count toward your housing payment, a careful DTI calculation is critical. A loan officer experienced in NoVA will know how to factor in HOA dues, condo fees, and supplemental tax assessments correctly during pre-approval — something national online lenders frequently mishandle.

Run the Numbers

What Will Your Monthly Payment Be?

Use our mortgage calculator to estimate your monthly payment for any home price in Virginia, Maryland, or DC.

How Long Pre-Approval Takes (and Lasts)

Time to Get Pre-Approved

For a borrower with straightforward W-2 income, clean credit, and ready documentation, a standard pre-approval takes 1–3 business days. For self-employed borrowers, military with complex pay structures, or anyone with recent credit events, plan on 3–7 business days. Underwritten pre-approval (TBD) adds another 2–5 business days on top.

The single biggest variable is how quickly you submit complete documentation. Lenders can't move faster than the documents arrive — and incomplete uploads (a missing pay stub page, a bank statement without all account numbers visible) push you to the back of the queue.

How Long Your Letter Lasts

Pre-approval letters are typically valid for 60–90 days from the date of issue. After that, your lender will need updated documentation — most importantly, fresh pay stubs and a refreshed credit report — to reissue. Credit reports themselves expire at 120 days, so even within the letter's stated validity, you may need to refresh credit before closing if your shopping window stretches.

If you got pre-approved early in your search and haven't found a home in 90 days, that's normal — just give your loan officer a heads-up about a week before your letter expires so they can reissue without slowing down an offer.

What's Inside a Pre-Approval Letter

A well-written pre-approval letter typically includes:

- Borrower name(s) and date of issue

- Maximum purchase price the borrower is qualified for

- Loan program (Conventional, FHA, VA, USDA, Jumbo)

- Loan amount and minimum down payment percentage

- Property type (single-family, condo, townhouse)

- Occupancy (primary residence, second home, investment)

- Documentation reviewed — a list confirming credit, income, and assets were verified

- Conditions — typically subject to acceptable appraisal, clear title, and no material change in financial situation

- Loan officer signature, NMLS number, and contact information

- Letter expiration date

Pro tip: Ask your loan officer for a letter showing the exact offer amount you're submitting — not your maximum approval. If your offer is $725,000 but your letter says you're approved up to $900,000, the seller knows you have room to come up. A property-specific letter at the offer price preserves your negotiating leverage.

Common Mistakes That Derail Pre-Approval

Once you're pre-approved, the goal is to keep your financial picture stable until closing. The following mistakes blow up loans every month — sometimes the day before settlement.

⚠️ Don't Do Any of This Between Pre-Approval and Closing

- Don't open new credit cards or take out new loans. A new tradeline changes your DTI and re-prices your loan.

- Don't finance a car. A $650/month car payment can knock $100,000+ off your purchase power overnight.

- Don't change jobs without telling your loan officer. A change to a similar W-2 role in the same field is usually fine; a switch to 1099, a new industry, or a probationary period can pause your loan.

- Don't make large undocumented deposits. Anything over ~50% of your monthly income from a non-payroll source needs a paper trail.

- Don't pay off old collections without asking first. Paying a charge-off can re-age the account and lower your score temporarily.

- Don't co-sign a loan for anyone. The co-signed debt counts against your DTI even if you're not making payments.

- Don't move money between accounts without telling your lender. Every transfer needs to be documented or it triggers questions in underwriting.

Ready to Start Your Search?

Browse Homes for Sale in Northern Virginia

Once you know your budget, explore available homes across Loudoun, Fairfax, Prince William, Arlington, and Alexandria.

What Happens After You're Pre-Approved

Pre-approval is the launch pad — not the destination. Here's what the typical 30–45 day journey from pre-approval to closing looks like in Northern Virginia:

- Connect with a local real estate agent who knows your target submarkets and can interpret listing dynamics in real time.

- Tour homes with your pre-approval letter ready — you can write an offer the same day you find the right home.

- Submit an offer with the pre-approval letter attached. Your agent and loan officer will coordinate so the listing agent gets a clear, professional package.

- Ratified contract. Once both parties sign, you typically have 5–10 days for inspection and 21–30 days for financing contingency.

- Lock your interest rate. Most rate locks are 30–60 days; your loan officer will help you choose the right window for your closing date.

- Order the appraisal (paid by you, ordered by the lender from an independent appraiser).

- Underwriting review. An underwriter examines every page of your file, verifies your employment one more time, and issues conditional approval.

- Clear conditions. Provide any final documentation requested — typically updated pay stubs and a verification of employment.

- Final approval and Closing Disclosure (CD). You'll receive your CD at least 3 business days before closing — review every line.

- Closing. Sign at the title company in Virginia, get your keys, and start unpacking.

Frequently Asked Questions

How long does mortgage pre-approval take in Northern Virginia?

For a standard W-2 borrower with complete documentation, pre-approval typically takes 1–3 business days. Self-employed or complex-income borrowers should plan on 3–7 days. An upgraded underwritten (TBD) pre-approval adds another 2–5 business days.

What credit score do I need to get pre-approved in Virginia?

Minimums vary by loan type: 620 for conventional, 580 for FHA (3.5% down), and typically 580–620 for VA loans (lender-set, since the VA itself doesn't impose a minimum). USDA loans typically require 640. Higher scores unlock substantially better pricing — a 740+ score versus a 660 score can mean a meaningfully lower rate on a conventional loan.

What's the difference between pre-qualification and pre-approval?

Prequalification is a verbal estimate based on unverified information you provide — no documentation, no credit pull. Pre-approval involves a hard credit pull, document verification (pay stubs, W-2s, bank statements), and a written letter committing to a specific loan amount. In Northern Virginia, only pre-approval is taken seriously by listing agents.

How long is a mortgage pre-approval letter good for?

Most pre-approval letters are valid for 60–90 days from the issue date. After that, your lender will need updated pay stubs and a refreshed credit report to reissue. Credit reports themselves expire after 120 days regardless of the letter's stated validity.

Does getting pre-approved hurt my credit score?

A mortgage credit pull is a hard inquiry and may temporarily reduce your score by a few points. However, FICO scoring treats multiple mortgage inquiries within a 45-day window as a single inquiry, so you can shop multiple lenders without compounding the credit impact. The benefit of pre-approval far outweighs the small temporary score impact.

What is the conforming loan limit in the DC metro area for 2026?

The 2026 conforming loan limit for the DC metro high-cost area is $1,249,125 for a single-family home. The FHA loan limit for the same area is $1,149,825. These limits are higher than the standard national limits because the DC metro is designated a high-cost area by the FHFA.

How much down payment do I need to get pre-approved?

Minimum down payments depend on loan type: 3% for conventional first-time buyer programs, 3.5% for FHA, 0% for VA (eligible veterans/active duty), and 0% for USDA (eligible rural areas). Virginia Housing's Down Payment Assistance Grant program can layer on additional help for qualifying borrowers.

Can I get pre-approved before I find a real estate agent?

Yes — and most experienced loan officers recommend it. Pre-approval first means you'll know your budget before you start touring homes, you can write a strong offer the moment you find the right property, and you won't fall in love with a home that's outside your qualifying range.

Can I be pre-approved with student loans?

Absolutely. Student loans are factored into your DTI ratio, but they don't disqualify you. The way each loan program treats deferred or income-driven repayment plans varies — Fannie Mae, Freddie Mac, FHA, and VA all have slightly different rules. A loan officer experienced with NoVA's high-income, high-debt buyer profile can often qualify you on a different program than the one you assumed.

What happens if I find a home that costs more than my pre-approval amount?

Talk to your loan officer immediately. There's often room to increase your approval by adjusting loan program, documenting additional income, or restructuring the down payment. If a higher amount truly isn't feasible, the loan officer will tell you — better to find out before you write the offer than after.

How do I find a good mortgage lender in Northern Virginia?

Look for an NMLS-licensed loan officer with deep local experience, transparent pricing, fast turn times, and references from agents and clients in the DMV. Confirm the lender is licensed in Virginia, Maryland, DC, and ideally West Virginia if you might broaden your search. Ken Byrne (NMLS #187129) at ALCOVA Mortgage LLC (NMLS #40508) is licensed across all four jurisdictions and specializes in Northern Virginia transactions including conventional, FHA, VA, USDA, and jumbo financing.

Is now a good time to get pre-approved in Northern Virginia?

Pre-approval itself costs nothing and creates no obligation. Even if you're 6+ months from buying, a pre-approval consultation will tell you exactly where you stand, what to fix on your credit, and how much to save — so when you're ready, you're already ahead. Inventory and rate environments change, but being ready to move when the right home appears is always valuable.

Mortgage Glossary

Automated Underwriting System (AUS): Software (Fannie Mae's DU or Freddie Mac's LPA) that evaluates your loan application against program guidelines and returns an approval recommendation.

Debt-to-Income Ratio (DTI): Total monthly debt obligations divided by gross monthly income, expressed as a percentage. The lower, the better.

Loan Estimate (LE): A standardized 3-page document your lender provides within 3 days of your application, showing the estimated loan terms, payments, and closing costs.

Conforming Loan: A loan that meets Fannie Mae or Freddie Mac guidelines, including loan amount limits set annually by the FHFA.

Jumbo Loan: A loan that exceeds the conforming loan limit. In the DC metro area, that means a loan above $1,249,125 for a single-family home in 2026.

Tri-Merge Credit Report: A combined credit report pulling data from all three bureaus — Equifax, Experian, and TransUnion — used by mortgage lenders.

TBD Approval: An underwritten pre-approval where the file has been fully reviewed by an underwriter except for property-specific conditions. Stronger than a standard pre-approval.

Closing Disclosure (CD): A final 5-page document summarizing the actual loan terms and costs at closing. By law, you must receive it at least 3 business days before settlement.

Buying & Selling at the Same Time?

Save Thousands When You List for 1.5%

If you're trading up, downsizing, or relocating, full-service listing at 1.5% commission can put thousands more in your pocket — money that goes straight to your next down payment.

Conclusion: Get Pre-Approved Before You Tour

In Northern Virginia, the buyers who close on the homes they want are almost always the ones who got pre-approved before they started touring. They know their budget, they know their loan options, they have their letter ready, and they can move on day one when the right home hits the market.

The process isn't complicated, it doesn't cost anything, and it doesn't commit you to anything. Spend an hour gathering documents, an hour with a local loan officer, and you'll know exactly where you stand — and exactly what to fix if there's anything in the way.

If you're ready to start, JB Financing — powered by ALCOVA Mortgage LLC — has been helping NoVA buyers navigate pre-approval for years. Ken Byrne (NMLS #187129) and the ALCOVA team are licensed in Virginia, Maryland, DC, and West Virginia and specialize in the loan structures that actually work for DMV buyers.

Free · No Commitment

Start Your Pre-Approval Today

A few minutes online today means you're ready to write an offer the moment you find the right home in Northern Virginia.

Ken Byrne NMLS #187129 · ALCOVA Mortgage LLC NMLS #40508

Disclaimer: This article is for informational purposes only and does not constitute financial or legal advice. Mortgage programs, rates, and eligibility requirements are subject to change. Contact a licensed mortgage professional for guidance specific to your situation. Ken Byrne, NMLS #187129 · ALCOVA Mortgage LLC, NMLS #40508 · Licensed in VA, MD, DC, WV.

Categories

Recent Posts

GET MORE INFORMATION

Broker Associate