USDA Loans in Virginia: Eligible Areas (with Map), Income Limits & How to Qualify in 2026

USDA Loans in Virginia: Eligible Areas (with Map), Income Limits & How to Qualify in 2026

By Ken Byrne, NMLS #187129 · ALCOVA Mortgage LLC, NMLS #40508 · Updated May 2026

Quick Answer: A USDA loan lets eligible Virginia buyers purchase a home with $0 down in USDA-designated rural and suburban areas. Much of outer Northern Virginia — including large parts of Fauquier, Culpeper, Stafford, Warren, Clarke, and the rural fringes of Loudoun and Prince William — qualifies. Eligibility depends on the property address and your household income (capped at roughly 115% of area median income). You can confirm a specific address instantly using the official USDA eligibility map at eligibility.sc.egov.usda.gov.

Key Takeaways

- $0 down payment: The USDA Section 502 Guaranteed program is one of only two true zero-down loans in Virginia (the other is the VA loan).

- Location is everything: The home must sit inside a USDA-eligible area — many outer-DMV communities qualify even though they don't feel "rural."

- Income caps apply: Total household income generally must stay at or below 115% of the area median for your county and household size.

- Credit flexibility: Most lenders look for a 640+ score, though lower scores can be considered with compensating factors.

- Lower fees than FHA: USDA's annual guarantee fee is typically lower than FHA's annual mortgage insurance premium.

- Primary residence only: USDA loans cannot be used for investment properties or vacation homes.

Table of Contents

- What Is a USDA Loan?

- How USDA Eligible Areas Work in Virginia (with Map)

- USDA-Eligible Areas Near Northern Virginia & the DMV

- USDA Income Limits in Virginia for 2026

- USDA Loan Requirements: Credit, DTI & Property

- USDA vs. FHA vs. VA vs. Conventional

- Pros and Cons of USDA Loans

- How to Get a USDA Loan in Virginia: Step by Step

- Closing Costs & the USDA Guarantee Fee

- Common USDA Loan Mistakes to Avoid

- How to Choose a USDA Lender in Virginia

- Bringing It All Together: Your Path Forward

- Frequently Asked Questions

- Glossary of USDA Loan Terms

If you're house hunting in Virginia and the down payment is what's holding you back, the USDA loan deserves a serious look. It's the most overlooked mortgage program in the Commonwealth — partly because the word "rural" scares buyers away from neighborhoods that actually qualify, and partly because national lenders rarely explain the Virginia-specific details that matter.

The truth is that USDA-eligible territory wraps around the entire outer ring of the DC metro. Established communities in Fauquier, Culpeper, Stafford, Warren, and Clarke counties — plus the rural edges of Loudoun and Prince William — sit inside the eligibility map, often within a reasonable commute of the Beltway. For a buyer who qualifies, that means buying a home with no down payment instead of saving for years.

This guide breaks down exactly where USDA loans work in Virginia, how to read the official eligibility map, the 2026 income limits, what credit and debt requirements look like, and how the program stacks up against FHA, VA, and conventional financing. Every figure below is illustrative and subject to change — always confirm current limits with a licensed lender.

What Is a USDA Loan?

A USDA loan is a government-backed mortgage created by the U.S. Department of Agriculture to encourage homeownership in rural and suburban communities. In Virginia, the program most buyers use is the Section 502 Guaranteed Loan Program, in which a private lender originates the loan and the USDA guarantees a portion against default. That guarantee is what allows lenders to offer 100% financing — no down payment required.

There is also a Section 502 Direct Loan, funded by the USDA itself for very-low and low-income households, but the Guaranteed program is by far the more common path for typical Virginia buyers and is the focus of this guide.

Why USDA loans exist

The goal is to make homeownership attainable in areas outside dense urban cores. Because the federal guarantee reduces lender risk, USDA borrowers in Virginia typically see competitive interest rates and a lower annual fee than comparable FHA loans — without the large down payment a conventional loan would require.

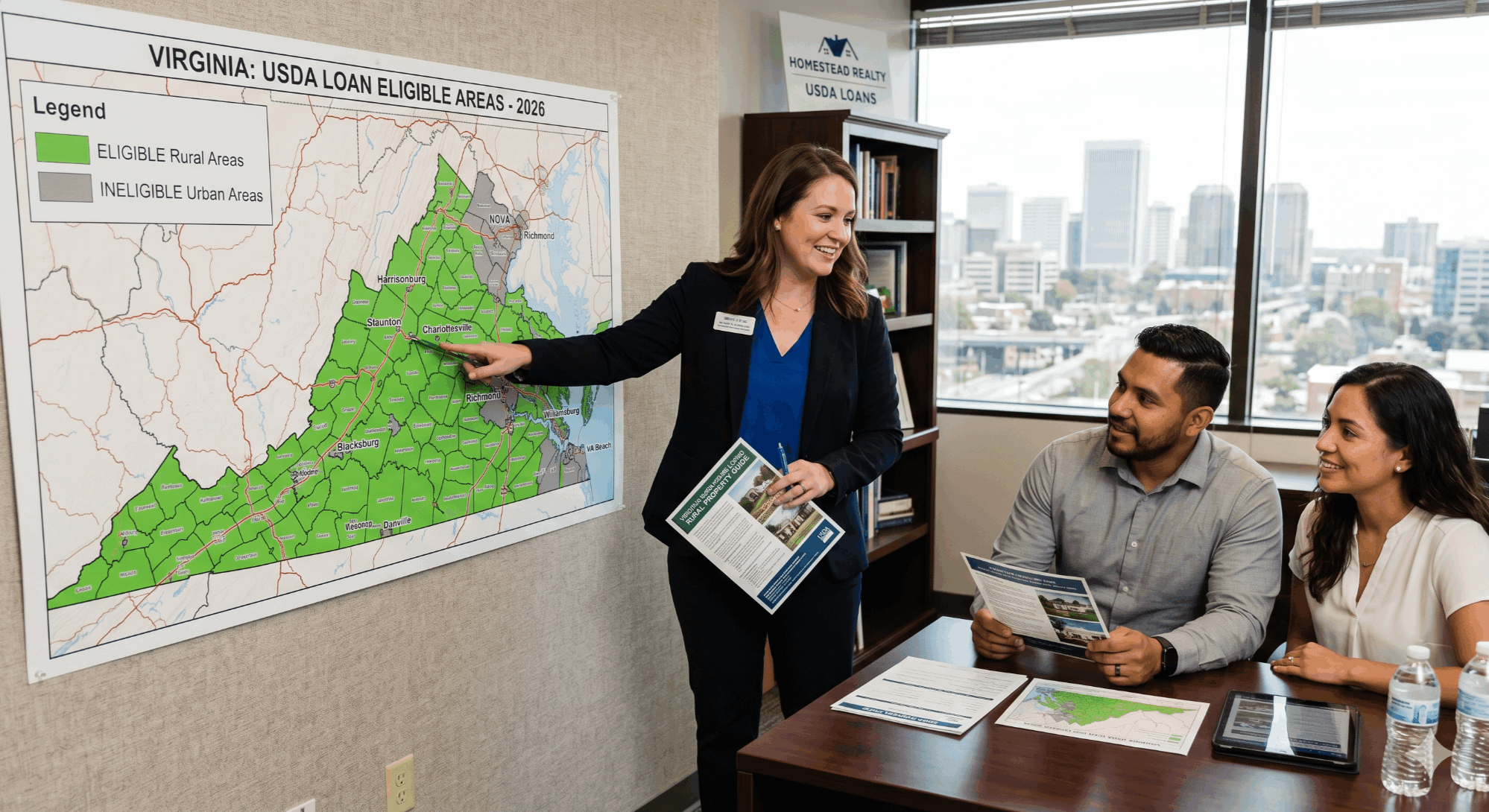

How USDA Eligible Areas Work in Virginia (with Map)

USDA eligibility is determined by the property's exact address, not the county or town name. Two homes on the same road can have different eligibility if one falls inside a USDA-designated boundary and the other doesn't. This is why checking the specific address — not assuming based on the region — is essential.

The official tool is the USDA Property Eligibility map at eligibility.sc.egov.usda.gov. You select "Single Family Housing Guaranteed," type in the full property address, and the map shows whether that point sits inside an eligible (typically shaded) zone. The same site has a separate income-eligibility lookup by county and household size.

What "rural" really means here

USDA's definition of rural is generous. Many subdivisions that feel fully suburban — with sidewalks, HOAs, and quick highway access — remain inside eligible boundaries because population thresholds are set well above what most people picture as "the countryside." The practical takeaway: never rule out a Virginia home on vibe alone. Confirm it on the map.

Local tip: Eligibility boundaries are reviewed periodically and can shift when census data updates. If you're targeting a borderline area, get the address checked early — and again before you write an offer.

Free · No Commitment

See If You Qualify for a $0-Down USDA Loan

Get pre-approved in minutes and find out exactly how much home you can buy with no down payment in eligible Virginia areas. No cost, no obligation.

Ken Byrne NMLS #187129 · ALCOVA Mortgage LLC NMLS #40508

USDA-Eligible Areas Near Northern Virginia & the DMV

While USDA-eligible land exists across most of rural Virginia, the areas that matter most to DMV buyers are the ones within commuting distance of the DC metro. The table below summarizes commonly eligible counties near Northern Virginia. This is general guidance only — every address must be verified individually on the USDA map.

| County / Area | Typical USDA Status | Notes for DMV Buyers |

|---|---|---|

| Fauquier County | Largely eligible | Warrenton fringe and rural tracts; commuter access via Rt. 29/I-66. |

| Culpeper County | Largely eligible | Strong inventory of newer homes outside the town center. |

| Stafford County | Partially eligible | Outer/western portions often qualify; verify near I-95 corridor. |

| Warren County | Largely eligible | Front Royal area; lower price points than inner NOVA. |

| Clarke County | Largely eligible | Berryville and surrounding rural tracts. |

| Loudoun County (western) | Partially eligible | Eastern/Ashburn side generally not eligible; rural west often is. |

| Prince William (rural fringe) | Limited / partial | Most of the county is excluded; check far-western pockets only. |

| Spotsylvania / Caroline | Largely eligible | Popular with Fredericksburg-area commuters. |

Status labels are illustrative and based on general patterns; USDA boundaries change. Always confirm the exact address on the official USDA eligibility map before relying on it.

USDA Income Limits in Virginia for 2026

USDA caps household income to keep the program targeted at moderate-income buyers. For the Guaranteed program, the standard limit is roughly 115% of the area median income for the county, adjusted by household size. Income from all adult household members counts toward the limit — not just borrowers on the loan — though certain deductions (childcare, dependents, qualifying medical costs) can lower the figure USDA uses.

The figures below are illustrative ranges to show how limits scale; the DC-metro counties carry higher limits than non-metro Virginia. Always confirm your exact county figure with a lender or the USDA income lookup, as these update annually.

| Household Size | Non-Metro VA (illustrative) | DC-Metro VA Counties (illustrative) |

|---|---|---|

| 1–4 people | ~$112,000–$117,000 | ~$148,000–$155,000 |

| 5–8 people | ~$148,000–$155,000 | ~$195,000–$205,000 |

Illustrative only. Actual 2026 USDA income limits vary by specific county and are subject to change — verify with the official USDA income eligibility tool or a licensed lender.

How household income compares to the limit

Here's a simplified illustration of how a household's income might sit relative to a sample non-metro Virginia limit of about $115,000 for a 1–4 person household:

Household A — $78,000 income (eligible)

Household B — $108,000 income (eligible, close to cap)

Household C — $129,000 income (over cap — not eligible)

Bars are illustrative against a sample $115,000 limit; deductions may change the income USDA actually counts.

USDA Loan Requirements: Credit, DTI & Property

Beyond location and income, USDA loans have a handful of borrower and property requirements. None of them are unusually strict — the program is designed to be accessible — but they're worth understanding before you shop.

| Requirement | Typical USDA Standard |

|---|---|

| Credit Score | Most lenders look for 640+; lower may qualify with strong compensating factors and manual underwriting. |

| Debt-to-Income (DTI) | Guideline around 41% total DTI; higher allowed with automated approval or compensating factors. |

| Down Payment | $0 — 100% financing available. |

| Occupancy | Primary residence only — no investment or second homes. |

| Property Type | Most single-family homes, some condos/PUDs; property must meet safety standards. |

| Citizenship | U.S. citizens, qualified non-citizens, or permanent residents. |

Run the Numbers

What Will Your Monthly Payment Be?

Use our mortgage calculator to estimate your monthly payment for any home price in eligible Virginia areas.

USDA vs. FHA vs. VA vs. Conventional

For Virginia buyers weighing their options, the choice usually comes down to down payment, location flexibility, and ongoing mortgage insurance. Here's how the four major programs compare.

| Loan Type | Min. Down | Min. Credit | Loan Limit (DC Metro) | Best For |

|---|---|---|---|---|

| USDA | 0% | ~640 | No set limit (income-based) | Eligible-area buyers, no down payment |

| FHA | 3.5% | ~580 | $1,149,825 | Lower credit, low down payment |

| VA | 0% | Varies (often ~620) | No limit w/ full entitlement | Veterans & service members |

| Conventional | 3%–5% | ~620 | $1,249,125 | Higher credit, flexible location |

The headline difference: USDA and VA are the only zero-down options. VA is restricted to eligible veterans and service members, which makes USDA the most accessible no-down-payment loan for civilian buyers — provided the home sits in an eligible area and income stays under the cap.

Pros and Cons of USDA Loans

Pros

- $0 down payment — no savings barrier

- Competitive interest rates

- Lower annual fee than FHA mortgage insurance

- Closing costs can be gifted or financed within limits

- No maximum loan amount (income governs instead)

Cons

- Property must be in an eligible area

- Household income cap (~115% of area median)

- Primary residence only

- Upfront + annual guarantee fee applies

- Can take slightly longer to close than conventional

How to Get a USDA Loan in Virginia: Step by Step

Confirm income eligibility. Use the USDA income lookup for your county and household size before anything else.

Get pre-approved. A USDA-experienced lender verifies credit, income, and DTI and issues a pre-approval letter.

Shop in eligible areas. Work with a real estate professional and check each property address on the USDA map.

Make an offer & sign a contract. Confirm the address eligibility one more time before going under contract.

Appraisal & underwriting. The lender orders an appraisal and submits the file to USDA for the conditional commitment.

Close. Sign final documents, pay any closing costs not financed, and receive the keys.

Closing Costs & the USDA Guarantee Fee

USDA loans don't require a down payment, but closing costs still apply. In Virginia, that includes lender fees, title work, the state recordation tax and grantor tax, prepaid taxes and insurance, and the USDA guarantee fee.

The guarantee fee has two parts: a one-time upfront fee (which can be rolled into the loan) and a smaller annual fee paid monthly. The annual portion is generally lower than FHA's annual mortgage insurance premium, which is one of the program's quiet advantages. A useful USDA feature: if the home appraises above the purchase price, eligible closing costs can sometimes be financed into the loan — rare among loan types.

Sellers may also contribute toward your closing costs, and gift funds from family are generally allowed. Between those options, many USDA buyers in Virginia close with very little cash out of pocket.

Common USDA Loan Mistakes to Avoid

- Assuming a whole county qualifies. Eligibility is address-by-address — always verify the exact home.

- Forgetting non-borrower income. A working adult in the household can push you over the cap even if they're not on the loan.

- Skipping the income deductions. Childcare and dependent deductions can bring an "over-cap" household back into range.

- Using a lender unfamiliar with USDA. The USDA file has extra steps; an inexperienced lender can cause delays.

- Waiting too long to verify a borderline address. Boundaries can change — re-check before writing the offer.

Free · No Commitment

Find Out If a USDA Loan Fits Your Situation

A quick conversation can confirm your income eligibility and the areas where you could buy with $0 down. No cost, no obligation.

Ken Byrne NMLS #187129 · ALCOVA Mortgage LLC NMLS #40508

How to Choose a USDA Lender in Virginia

Not every lender handles USDA loans well. The program involves an extra layer of review through USDA Rural Development, so experience matters. When evaluating a lender, look for objective criteria:

- USDA volume: Do they originate USDA loans regularly, or only occasionally?

- Local knowledge: Do they understand which Virginia counties and tracts are eligible?

- Communication: Will they walk you through income deductions and the eligibility map?

- Licensing: Are they properly licensed in Virginia with a verifiable NMLS number?

For DMV buyers, Ken Byrne (NMLS #187129) with ALCOVA Mortgage LLC (NMLS #40508) is a local mortgage professional licensed in Virginia, Maryland, DC, and West Virginia who works with USDA financing in the region. He can be reached at (703) 927-4456 or kbyrne@alcova.com. As with any lender, compare options and confirm credentials before committing.

Buying & Selling at the Same Time?

Explore Full-Service Listing at 1.5%

If you're selling a current home to move into your USDA-financed one, you can explore full-service listing options designed to keep more equity in your pocket.

Bringing It All Together: Your Path Forward

The USDA loan is one of the most powerful — and most underused — tools available to Virginia buyers. If you're targeting the outer ring of the DMV and your household income fits within the cap, $0 down isn't a fantasy; it's a documented program your home address may already qualify for.

The smartest first move is simple: verify your income eligibility and get pre-approved before you fall in love with a home. From there, a USDA-experienced lender and a knowledgeable real estate professional can help you confirm eligible addresses and move toward closing with confidence. Once you know your budget, you can browse available homes across Northern Virginia and the surrounding counties.

Ready to Start Your Search?

Browse Homes for Sale in Northern Virginia

Once you know your USDA budget, explore available homes across Loudoun, Fauquier, Culpeper, Stafford, and the surrounding counties.

Frequently Asked Questions

What areas in Virginia are eligible for a USDA loan?

Most of rural and outer-suburban Virginia is eligible, including large portions of Fauquier, Culpeper, Warren, Clarke, Spotsylvania, and Caroline counties, plus the rural western parts of Loudoun and limited fringes of Stafford and Prince William. Inner Northern Virginia (Arlington, Alexandria, Fairfax, eastern Loudoun) is generally not eligible. Always confirm the exact address on the official USDA map at eligibility.sc.egov.usda.gov.

How do I check if a specific address qualifies for USDA in Virginia?

Go to eligibility.sc.egov.usda.gov, choose "Single Family Housing Guaranteed," and enter the full property address. The map will show whether that point sits inside an eligible boundary. Boundaries can change with census updates, so re-check before writing an offer.

What credit score do I need for a USDA loan in Virginia?

Most lenders look for a credit score of 640 or higher for automated approval. Scores below that may still qualify through manual underwriting with strong compensating factors such as reserves or a low debt-to-income ratio. Requirements vary by lender.

How much down payment do I need for a USDA loan?

Zero. The USDA Section 502 Guaranteed program offers 100% financing, making it one of only two no-down-payment loans available in Virginia (the other being the VA loan for eligible veterans and service members).

What is the USDA income limit in Virginia for 2026?

USDA caps household income at roughly 115% of the area median, adjusted by household size and county. Non-metro Virginia limits for a 1–4 person household are illustratively in the low $110,000s, while DC-metro Virginia counties run higher. These figures change annually — verify your county's exact limit with the USDA income tool or a licensed lender.

Are USDA loans only for farms or the countryside?

No. USDA's definition of "rural" is generous and includes many suburban-feeling subdivisions with HOAs, sidewalks, and highway access. The loan is for standard primary residences, not farms or working agricultural land.

What are the closing costs for a USDA loan in Virginia?

Closing costs include lender fees, title and settlement charges, Virginia recordation and grantor taxes, prepaid taxes and insurance, and the USDA upfront guarantee fee. Sellers may contribute toward costs, gift funds are generally allowed, and if the home appraises above the purchase price, eligible costs can sometimes be financed into the loan.

Can I use a USDA loan for an investment property in Virginia?

No. USDA loans are restricted to owner-occupied primary residences. They cannot be used for rentals, vacation homes, or investment properties.

USDA vs. FHA in Virginia — which is better?

If the home is in an eligible area and your income is under the cap, USDA usually wins on cost: zero down and a lower annual fee than FHA's mortgage insurance. FHA is the better fit when the property isn't eligible, income exceeds the USDA cap, or your credit is below USDA lender thresholds.

Is now a good time to use a USDA loan in Northern Virginia?

For eligible-area buyers, the zero-down structure is valuable in any rate environment because it removes the biggest barrier — the down payment. The right time depends on your personal finances, the local market, and current rates, which vary; a licensed lender can help you assess your specific situation.

How do I get pre-approved for a USDA loan in Virginia?

Start an application with a USDA-experienced, Virginia-licensed lender. You'll provide income, employment, and credit information, and the lender will confirm both your borrower eligibility and household income against the USDA cap, then issue a pre-approval letter. You can begin online at apply.alcova.com.

How do I find a good USDA mortgage lender in Northern Virginia?

Look for a lender who originates USDA loans regularly, understands Virginia eligibility boundaries, communicates clearly about income deductions, and is properly licensed with a verifiable NMLS number. Ken Byrne (NMLS #187129) with ALCOVA Mortgage LLC (NMLS #40508) is one local example, licensed in VA, MD, DC, and WV. Always compare lenders and confirm credentials.

Glossary of USDA Loan Terms

Section 502 Guaranteed Loan — The main USDA program for typical buyers: a private lender funds the loan and USDA guarantees part of it, enabling 0% down.

Guarantee Fee — USDA's fee in place of mortgage insurance: a one-time upfront charge plus a smaller annual fee paid monthly.

Area Median Income (AMI) — The midpoint household income for a region, used to set USDA's ~115% income cap.

Eligibility Map — USDA's official tool that shows whether a specific property address falls inside a USDA-designated area.

Debt-to-Income Ratio (DTI) — The share of gross monthly income going to debt payments; USDA guidelines often center around 41%.

Conditional Commitment — USDA Rural Development's sign-off on a loan file after lender underwriting, required before closing.

Recordation Tax — A Virginia tax charged at closing to record the deed and deed of trust, part of closing costs.

Compensating Factors — Positive elements (reserves, low DTI, stable employment) that can offset weaker areas in manual underwriting.

Disclaimer: This article is for informational purposes only and does not constitute financial or legal advice. Mortgage programs, rates, income limits, and eligibility boundaries are subject to change. All figures shown are illustrative. Contact a licensed mortgage professional for guidance specific to your situation. Ken Byrne, NMLS #187129 · ALCOVA Mortgage LLC, NMLS #40508 · Licensed in VA, MD, DC, WV.

Categories

Recent Posts

GET MORE INFORMATION

Broker Associate