VA Loan Limits in Virginia, Maryland, DC, and West Virginia (2026 Guide)

VA Loan Limits in Virginia, Maryland, DC, and West Virginia (2026 Guide)

By Ken Byrne, NMLS #187129 · ALCOVA Mortgage LLC, NMLS #40508 · Updated May 2026

Quick Answer: If you have full VA entitlement, there is no VA loan limit in 2026 — you can borrow as much as a lender approves with $0 down. VA loan limits only apply if you have reduced (partial) entitlement, in which case the cap matches the local conforming loan limit: $832,750 in most of Virginia and West Virginia, and $1,249,125 across the high-cost Washington DC metro (Northern Virginia, DC, suburban Maryland, and Jefferson County, WV).

Key Takeaways

- No limit with full entitlement: Since 2020, eligible veterans with full entitlement face no VA loan cap and need no down payment.

- Limits only matter with partial entitlement: A current VA loan or a prior VA foreclosure reduces your entitlement and reintroduces a cap.

- DC metro is high-cost: Northern Virginia, DC, and the Maryland suburbs use the $1,249,125 limit — not the $832,750 baseline.

- West Virginia split: Jefferson County (WV) falls in the DC-metro high-cost area; most other WV counties use the $832,750 baseline.

- You can buy above the limit: A "VA jumbo" is possible with a down payment of roughly 25% of the amount over your remaining entitlement.

- Entitlement can be restored: Selling a home or doing a one-time restoration can return you to full entitlement.

Table of Contents

- Do VA Loans Even Have Limits in 2026?

- Full Entitlement vs. Reduced Entitlement

- 2026 VA Loan Limits by State & County

- How VA Entitlement Actually Works

- VA Loan Limits vs. Conforming Loan Limits

- What This Means in High-Cost DMV Markets

- VA Loans vs. Other Loan Programs

- Calculating Your Limit With Reduced Entitlement

- Buying Above the Limit: VA Jumbo & Down Payment

- Common VA Loan Limit Mistakes

- How to Use Your VA Loan Benefit in the DMV

- Making the Most of Your VA Loan Benefit

- Frequently Asked Questions

- VA Loan Glossary

If you're a service member, veteran, or surviving spouse shopping for a home in the DMV, "What's my VA loan limit?" is one of the first questions you'll ask — and the answer surprises most people. For the majority of qualified borrowers in 2026, the honest answer is that there is no limit. The VA loan limit only re-enters the picture in specific situations, and understanding when it applies can be the difference between a clean $0-down purchase and an unexpected down payment requirement in a market like Arlington, Bethesda, or the West Virginia panhandle.

This guide breaks down exactly how VA loan limits work across Virginia, Maryland, Washington DC, and West Virginia for 2026 — including the high-cost DC-metro figures that national sites frequently get wrong — so you can walk into a pre-approval conversation knowing precisely where you stand.

Do VA Loans Even Have Limits in 2026?

For most eligible borrowers, no. The Blue Water Navy Vietnam Veterans Act, effective January 1, 2020, eliminated VA loan limits for veterans and service members with full entitlement. That change is still in force in 2026. If you have full entitlement, the VA places no ceiling on how much you can borrow with zero down — the only ceiling is what a lender will approve based on your income, credit, and debt-to-income ratio.

This matters enormously in the DMV, where median prices in many Northern Virginia and suburban Maryland communities sit well above the national baseline. A full-entitlement borrower in Loudoun County can buy a $900,000 home with no down payment and no "limit" standing in the way — something that simply wasn't possible before 2020.

The phrase "VA loan limit" still exists, though, because it applies to borrowers with reduced entitlement. That's the group this guide spends the most time on, because the rules there are genuinely confusing and a small miscalculation can cost thousands.

Full Entitlement vs. Reduced Entitlement

Everything about VA loan limits comes down to one question: do you have full entitlement or reduced entitlement? Here's how to tell.

| Scenario | Entitlement Status | Loan Limit Applies? |

|---|---|---|

| You've never used a VA loan | Full | No |

| You used a VA loan but sold the home and repaid it in full | Full (restored) | No |

| You currently have an active VA loan | Reduced | Yes |

| You had a VA loan foreclosure or short sale (entitlement not restored) | Reduced | Yes |

| You're buying a second home while keeping a VA-financed first home | Reduced | Yes |

In plain terms: if you've never used your VA benefit, or you've fully restored it, you have no loan limit. If part of your entitlement is tied up in another loan or a past loss, the limit comes back — and it's tied to the conforming loan limit for the county where you're buying.

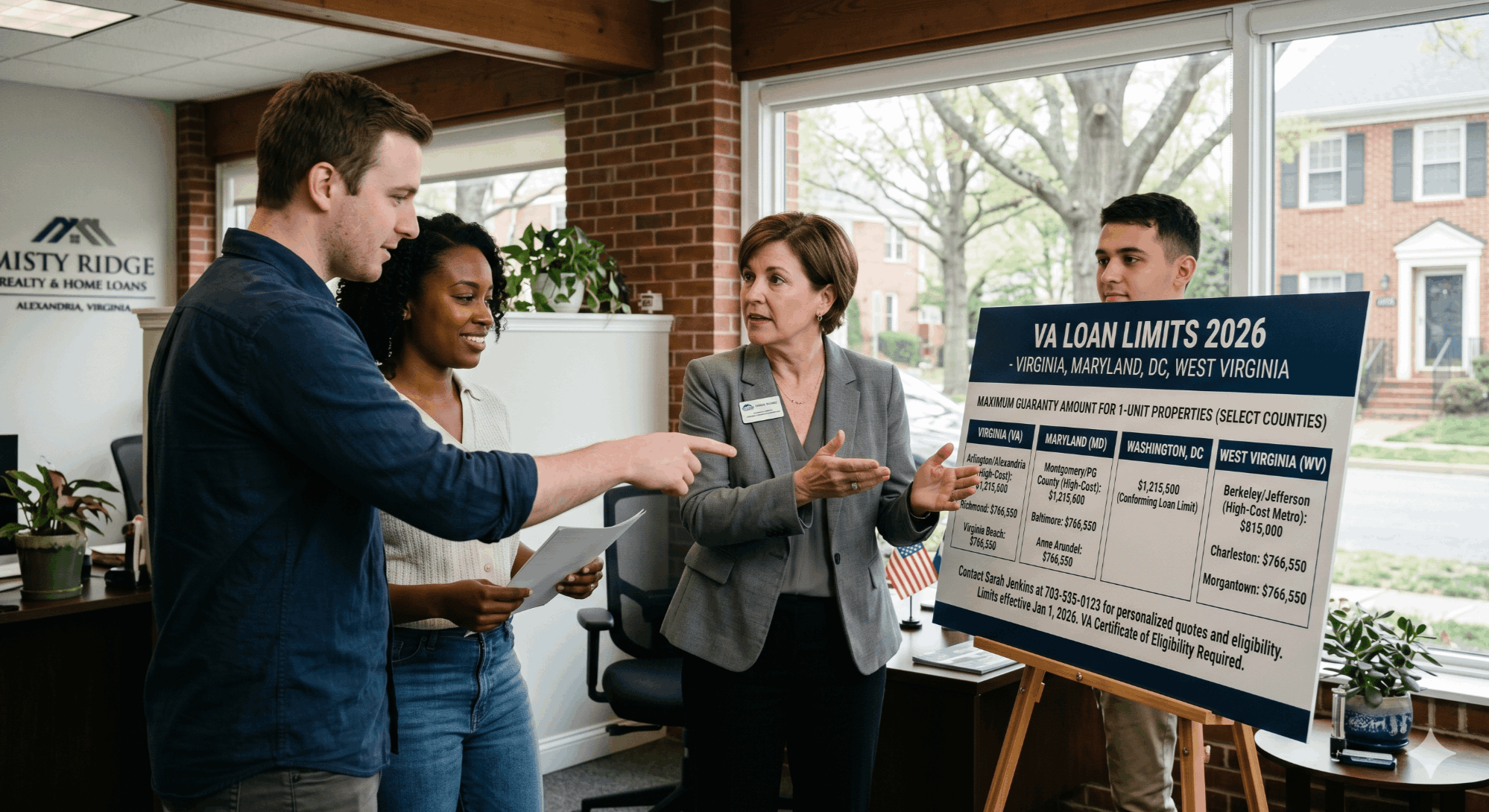

2026 VA Loan Limits by State & County

For borrowers with reduced entitlement, the 2026 VA loan limit equals the FHFA conforming loan limit for the county. There are two tiers across the DMV: the national baseline and the high-cost Washington-Arlington-Alexandria metro figure.

| Area | 2026 Limit (1-Unit) | Tier |

|---|---|---|

| Washington DC | $1,249,125 | High-cost |

| Northern VA — Arlington, Fairfax, Loudoun, Prince William, Alexandria, Falls Church, Fairfax City, Manassas, Stafford, Spotsylvania, Fauquier, Culpeper, Clarke, Warren, Rappahannock, Fredericksburg | $1,249,125 | High-cost |

| Rest of Virginia — Richmond, Virginia Beach, Roanoke, Charlottesville, etc. | $832,750 | Baseline |

| Suburban MD (DC metro) — Montgomery, Prince George's, Frederick, Charles, Calvert | $1,249,125 | High-cost |

| Rest of Maryland — Baltimore-area & other counties | $832,750 | Baseline |

| Jefferson County, WV (DC metro) | $1,249,125 | High-cost |

| Rest of West Virginia — Berkeley, Kanawha, Monongalia, etc. | $832,750 | Baseline |

County designations follow FHFA's 2026 conforming loan limit values. Confirm your specific county before you write an offer — a single county line can move you between the $832,750 and $1,249,125 tiers.

Free · No Commitment

See What You Qualify For Today

Find out exactly how much of your VA entitlement is available and how much home you can buy in the DMV — with no cost and no obligation.

Ken Byrne NMLS #187129 · ALCOVA Mortgage LLC NMLS #40508

How VA Entitlement Actually Works

Entitlement is the dollar amount the VA guarantees to your lender if you default. It comes in two layers:

Basic Entitlement

Every eligible borrower starts with $36,000 of basic entitlement. On its own this is small, but it's only part of the picture.

Bonus (Tier 2) Entitlement

On top of basic entitlement, the VA adds bonus entitlement equal to 25% of the county conforming loan limit. In a baseline county that's 25% of $832,750; in the high-cost DC metro it's 25% of $1,249,125. Lenders generally want the VA guaranty to cover 25% of the loan, which is why these figures act as the practical "limit" for reduced-entitlement borrowers.

With full entitlement, the VA effectively backs 25% of whatever you borrow with no cap — which is why no down payment and no limit apply. With reduced entitlement, only your remaining entitlement is available, and that's where math becomes necessary.

VA Loan Limits vs. Conforming Loan Limits

A common point of confusion: the VA does not publish its own loan limit table. For reduced-entitlement borrowers, it simply borrows the FHFA conforming loan limit. The chart below shows how far apart the two DMV tiers are.

Baseline (most of VA / WV / MD) — $832,750

High-cost DC metro (NoVA / DC / suburban MD / Jefferson Co. WV) — $1,249,125

That ~$416,000 gap is the single biggest reason national mortgage sites mislead DMV veterans — many quote only the $832,750 baseline and never mention that Northern Virginia, DC, and the Maryland suburbs sit in the high-cost tier.

What This Means in High-Cost DMV Markets

The DMV is one of the most VA-loan-heavy markets in the country thanks to the Pentagon, Fort Belvoir, Quantico, Joint Base Andrews, and the constant PCS relocation cycle. Here's the practical takeaway by buyer type:

- First-time VA buyer (full entitlement): No limit. You can target homes well into seven figures in Arlington or Bethesda with $0 down, subject only to income and DTI.

- PCS buyer keeping a prior VA home: Reduced entitlement. Your remaining entitlement is calculated against the $1,249,125 DC-metro figure if you're buying in NoVA, DC, or suburban Maryland.

- Buyer relocating to the WV panhandle: Jefferson County uses the high-cost $1,249,125 figure; Berkeley County and most of WV use the $832,750 baseline.

Run the Numbers

What Will Your Monthly Payment Be?

Estimate your monthly VA loan payment for any price point in Virginia, Maryland, DC, or West Virginia.

VA Loans vs. Other Loan Programs

For eligible borrowers, the VA loan is usually the strongest option in the DMV. Here's how it stacks up in 2026.

| Loan Type | Min. Down | Min. Credit | Loan Limit (DC Metro) | Best For |

|---|---|---|---|---|

| VA (full entitlement) | 0% | Lender-set (often 580–620) | No limit | Eligible vets/service members |

| VA (reduced entitlement) | Varies | Lender-set | $1,249,125 | Vets with an existing VA loan |

| Conventional | 3%–5% | 620+ | $1,249,125 | Strong-credit, non-veteran buyers |

| FHA | 3.5% | 580 | $1,149,825 | Lower-credit / low-down buyers |

| USDA | 0% | 640 typical | Income-based | Rural-eligible VA/WV areas |

Credit minimums shown are common lender overlays, not VA-mandated. Rates vary; current rates are available through your lender.

Calculating Your Limit With Reduced Entitlement

If you have reduced entitlement, here's the step-by-step logic a lender uses to determine how much you can borrow with $0 down — and where a down payment kicks in.

Identify your county's 2026 limit — $832,750 baseline or $1,249,125 high-cost (DC metro).

Multiply that limit by 25% to find your maximum guaranty (e.g., $1,249,125 × 25% = $312,281).

Subtract the entitlement already tied up in your existing VA loan to find your remaining guaranty.

Multiply the remaining guaranty by 4 to find the maximum you can finance with $0 down.

For any amount above that, expect a down payment of roughly 25% of the overage.

This math is genuinely easy to get wrong, especially when a prior loan was in a different county tier. Having a lender run it before you make an offer prevents an ugly surprise at underwriting.

Buying Above the Limit: VA Jumbo & Down Payment

A "VA jumbo" isn't a separate program — it's a VA loan above your available zero-down threshold. With full entitlement, there's no jumbo threshold at all; lender approval is the only ceiling. With reduced entitlement, a purchase above your remaining-entitlement cap generally requires a down payment equal to about 25% of the amount over that cap — far less than the 10–20% a conventional jumbo would demand.

In a high-cost market like McLean or Potomac, that 25%-of-the-overage structure is one of the most underused advantages available to veterans. The down payment is dramatically smaller than most borrowers assume.

Ready to Start Your Search?

Browse Homes for Sale in Northern Virginia

Once you know your VA buying power, explore available homes across Loudoun, Fairfax, Prince William, Arlington, and Alexandria.

Common VA Loan Limit Mistakes

- ✕ Assuming there's a $832,750 cap when you actually have full entitlement and no cap at all.

- ✕ Using the baseline figure in a high-cost county — NoVA, DC, suburban MD, and Jefferson Co. WV use $1,249,125.

- ✕ Forgetting to restore entitlement after selling a prior VA-financed home.

- ✕ Believing a VA jumbo requires 20% down — it's roughly 25% of the overage only, or nothing with full entitlement.

- ✕ Not pulling your Certificate of Eligibility (COE) before house hunting.

How to Use Your VA Loan Benefit in the DMV

Request your Certificate of Eligibility (COE) — your lender can usually pull it instantly.

Confirm whether you have full or reduced entitlement.

Get pre-approved so you know your true buying power and county tier.

Shop within your approved range with a licensed local real estate professional.

Lock your terms and close — VA loans often have no PMI and competitive rates.

Making the Most of Your VA Loan Benefit

The headline for 2026 is simple: most DMV veterans have no VA loan limit. Full entitlement means you can compete in Northern Virginia, DC, and the Maryland suburbs with $0 down and no ceiling beyond what your income supports. Limits only re-enter the picture with reduced entitlement — and even then, the high-cost $1,249,125 figure gives you far more room than national sites suggest. The most expensive mistake is assuming a cap that doesn't apply to you, or using the baseline number in a high-cost county.

If you're also selling a current home as part of a PCS or upsize, it's worth exploring full-service listing options that keep more equity in your pocket for the next purchase.

Free · No Commitment

Confirm Your VA Buying Power

Get pre-approved and find out exactly how much home your entitlement supports in the DMV market.

Ken Byrne NMLS #187129 · ALCOVA Mortgage LLC NMLS #40508

Selling As You Buy?

List Your Current Home for 1.5%

If a PCS or upsize means selling your current home, a full-service 1.5% listing keeps more equity available for your next VA purchase.

Frequently Asked Questions

Is there a VA loan limit in Virginia for 2026?

Not for borrowers with full entitlement — there is no limit. For those with reduced entitlement, the cap is $832,750 in most of Virginia and $1,249,125 in the Northern Virginia DC-metro counties.

What is the VA loan limit in the Washington DC metro for 2026?

For reduced-entitlement borrowers, $1,249,125 — the high-cost conforming limit covering DC, Northern Virginia, suburban Maryland, and Jefferson County, WV. Full-entitlement borrowers have no limit.

What credit score do I need for a VA loan in Virginia?

The VA sets no minimum, but most lenders look for roughly 580–620. Stronger credit can improve your rate and approval odds.

How much down payment do I need for a VA loan in Northern Virginia?

With full entitlement, $0 — even on high-priced NoVA homes. With reduced entitlement, you may owe about 25% of any amount above your remaining-entitlement cap.

Do VA loans have a limit in West Virginia?

For reduced entitlement: Jefferson County uses the high-cost $1,249,125 figure (it's in the DC metro), while Berkeley County and most of West Virginia use the $832,750 baseline. Full entitlement means no limit statewide.

What is the VA loan limit in Maryland for 2026?

Reduced-entitlement borrowers in the DC-metro Maryland counties (Montgomery, Prince George's, Frederick, Charles, Calvert) use $1,249,125; most other Maryland counties use the $832,750 baseline.

Can I have two VA loans at the same time?

Yes. This typically means reduced entitlement on the second loan, with your county's conforming limit determining how much you can finance with no down payment.

How do I restore my full VA entitlement?

Selling the home and paying off the VA loan in full usually restores entitlement; a one-time restoration is also available if you've paid off the loan but kept the home. Your lender can verify your status via your COE.

How do I get pre-approved for a VA loan in the DMV?

Start an application with a VA-experienced lender, who will pull your COE, confirm entitlement, and verify income and credit. You can begin a no-cost pre-approval with Ken Byrne, NMLS #187129, at ALCOVA Mortgage LLC, NMLS #40508.

Is now a good time to use a VA loan in Northern Virginia?

With no down payment, no PMI, and no limit on full entitlement, the VA loan remains one of the strongest tools in a high-cost market. Rates vary, so confirm current pricing with your lender.

What are the closing costs for a VA loan in Virginia?

Expect the VA funding fee (unless exempt) plus standard Virginia costs such as recordation tax, grantor tax, title, and lender fees. The VA limits certain fees veterans can be charged.

How do I find a good VA mortgage lender in the DMV?

Look for a licensed lender with deep VA experience, local DMV knowledge, transparent fees, and responsive communication. Ken Byrne (NMLS #187129) at ALCOVA Mortgage LLC (NMLS #40508) is licensed in VA, MD, DC, and WV and works with DMV military buyers.

VA Loan Glossary

Entitlement: The dollar amount the VA guarantees to your lender, determining how much you can borrow with no down payment.

Full Entitlement: Status in which no VA loan limit applies — available if you've never used the benefit or have fully restored it.

Reduced (Partial) Entitlement: Status when some entitlement is tied to an existing VA loan or a past loss; a county-based limit applies.

Certificate of Eligibility (COE): The official document confirming your VA loan eligibility and entitlement status.

Conforming Loan Limit: The FHFA-set cap that VA borrowing limits are tied to for reduced-entitlement borrowers.

High-Cost Area: A county where home values push the limit to $1,249,125 in 2026 — including the DC metro.

VA Funding Fee: A one-time fee that helps sustain the program; some veterans (e.g., those with a service-connected disability) are exempt.

VA Jumbo: A VA loan above your zero-down threshold — no jumbo applies with full entitlement.

Disclaimer: This article is for informational purposes only and does not constitute financial or legal advice. Mortgage programs, rates, and eligibility requirements are subject to change. Contact a licensed mortgage professional for guidance specific to your situation. Ken Byrne, NMLS #187129 · ALCOVA Mortgage LLC, NMLS #40508 · Licensed in VA, MD, DC, WV.

Categories

Recent Posts

GET MORE INFORMATION

Broker Associate