How Much Is a Mortgage on a $600,000 House? What to Expect in the DMV

How Much Is a Mortgage on a $600,000 House? What to Expect in the DMV

By Ken Byrne, NMLS #187129 · ALCOVA Mortgage LLC, NMLS #40508 · Updated for 2026

A $600,000 house is the new median in much of the DMV — typical for single-family homes in Loudoun, parts of Fairfax, Frederick County (MD), Prince William, and many DC condos. But the price tag alone tells you very little about what you'll actually pay each month. Your true cost depends on your down payment, loan type, property taxes, insurance, mortgage insurance, and HOA dues. Two buyers purchasing the same $600,000 home can end up with monthly payments that differ by more than $1,200.

This guide breaks down exactly what a mortgage on a $600,000 house costs in 2026 — every line item, every loan type, and every down payment scenario — so you can budget with confidence before you write an offer in Northern Virginia, Maryland, or DC.

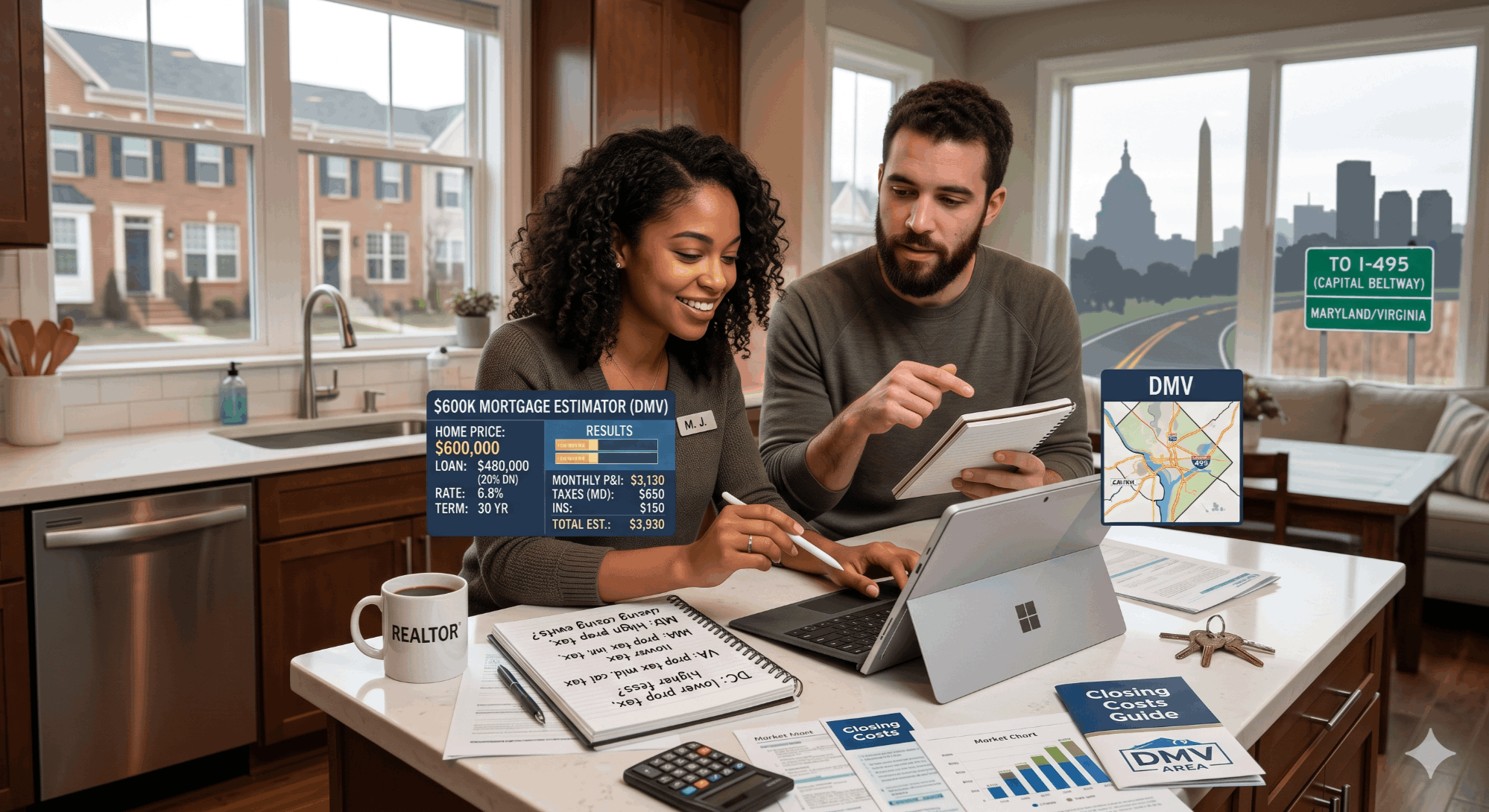

Quick Answer: A mortgage on a $600,000 house typically runs $3,900–$4,950 per month in the DMV when you include principal, interest, property taxes, homeowners insurance, and mortgage insurance. With 20% down ($120,000), expect roughly $4,000/month total. With 5% down on a conventional loan, total payment runs closer to $4,800/month including PMI. To comfortably afford a $600,000 home, most buyers need a household income of $150,000–$185,000 depending on debt and down payment.

Key Takeaways

- Principal & interest on a $600,000 home with 20% down is roughly $3,193/month at a 7% rate; with 5% down it rises to about $3,792/month.

- Property taxes in Northern Virginia add roughly $500–$580/month; Maryland counties run $480–$600/month; DC adds about $425/month at the standard rate.

- Homeowners insurance averages $145–$215/month for a $600,000 home in the DMV.

- PMI or MIP can add $170–$400/month if your down payment is below 20%.

- VA and USDA loans require 0% down, eliminating PMI entirely (though VA has a one-time funding fee).

- Closing costs in Virginia typically run $13,000–$22,000 on a $600,000 purchase, with the recordation tax being a notable Virginia-specific line item.

- Income to comfortably qualify: $150,000–$185,000 for most buyers, though VA buyers and those with lower debt can qualify with less.

Table of Contents

- The Five Parts of a Mortgage Payment (PITI + HOA)

- Payment by Down Payment: 3%, 5%, 10%, 20%

- Payment by Loan Type: Conventional, FHA, VA, USDA

- What Income Do You Need to Afford a $600,000 House?

- Closing Costs on a $600,000 Home in VA, MD, and DC

- Property Taxes by DMV County

- How Interest Rates Change Your Payment

- Total Cost Over 30 Years

- 7 Ways to Lower Your $600,000 Mortgage Payment

- Frequently Asked Questions

- Glossary of Mortgage Terms

The Five Parts of a Mortgage Payment (PITI + HOA)

Most homebuyers focus on the principal and interest figure their lender quotes — but that's only part of what you'll actually pay each month. Your full housing payment is known as PITI: Principal, Interest, Taxes, and Insurance — plus HOA dues and mortgage insurance when applicable. Here's what each component looks like for a $600,000 house.

1. Principal & Interest (P&I)

This is the portion of your payment that pays down the loan balance and the cost of borrowing. It's set by your loan amount, interest rate, and loan term (typically 30 years). On a $480,000 loan (a $600,000 home with 20% down) at a hypothetical 7% rate, P&I works out to roughly $3,193 per month. Your actual rate will vary — current rates are available through your lender.

2. Property Taxes (T)

Local jurisdictions assess property taxes annually, but lenders typically collect 1/12 of the total each month and hold it in escrow. For a $600,000 house, this ranges from about $425/month in DC up to $580/month in Fairfax County — a swing of more than $1,800/year just based on jurisdiction.

3. Homeowners Insurance (I)

Required by every lender. For a $600,000 home in the DMV, expect to pay about $1,750–$2,600 annually ($145–$215/month). Premiums vary by structure type, age of home, claims history, and credit score.

4. Mortgage Insurance (PMI or MIP)

If your down payment is below 20%, conventional loans require Private Mortgage Insurance (PMI). FHA loans require Mortgage Insurance Premium (MIP) regardless of down payment. PMI typically ranges from 0.3%–1.0% of the loan amount annually, depending on credit score and down payment. On a $570,000 conventional loan with 5% down, PMI alone can add $240–$380 per month.

5. HOA / Condo Dues

Common in DMV master-planned communities (Brambleton, Broadlands, Reston, One Loudoun, National Harbor) and in DC condos. HOA dues range from $100–$400/month for single-family homes and $400–$900/month for condos. Lenders count this toward your debt-to-income ratio (DTI) when qualifying you, even though it isn't part of "PITI" technically.

Free · No Commitment

See What You Qualify For Today

Get pre-approved in minutes and know exactly how much home you can afford in the DC metro market. No cost, no obligation.

Ken Byrne NMLS #187129 · ALCOVA Mortgage LLC NMLS #40508

Payment by Down Payment: 3%, 5%, 10%, 20%

Down payment is the single biggest lever you control. The table below shows how a $600,000 home payment changes by down payment, assuming a hypothetical 7% interest rate, $1,950/year homeowners insurance, $6,000/year property taxes (NOVA average), and standard PMI rates for conventional financing.

| Down Payment | Cash Required | Loan Amount | P&I | PMI | Est. Total PITI |

|---|---|---|---|---|---|

| 3% Conventional | $18,000 | $582,000 | $3,872 | $388 | $4,923 |

| 5% Conventional | $30,000 | $570,000 | $3,792 | $285 | $4,740 |

| 10% Conventional | $60,000 | $540,000 | $3,593 | $180 | $4,436 |

| 20% Conventional | $120,000 | $480,000 | $3,193 | $0 | $3,856 |

Estimates assume a hypothetical 7% interest rate, NOVA-average property taxes, and standard insurance. Actual rates and PMI vary by borrower.

The difference between 5% down and 20% down is roughly $884/month — but it requires an extra $90,000 in cash up front. Most DMV buyers find the math favors getting into the home sooner with less down and refinancing or eliminating PMI as the home appreciates.

Down Payment Visualized

3% down — $18,000

5% down — $30,000

10% down — $60,000

20% down — $120,000

Payment by Loan Type: Conventional, FHA, VA, USDA

The loan program you choose has just as much impact as your down payment. Here's how a $600,000 purchase compares across the four main loan types in the DMV.

| Loan Type | Min. Down | Min. Credit | Mortgage Insurance | Best For |

|---|---|---|---|---|

| Conventional | 3%–5% | 620 | PMI (drops at 78%) | Strong credit, flexibility |

| FHA | 3.5% | 580 | MIP (life of loan if <10% down) | Lower credit, smaller down |

| VA | 0% | 620 | None (one-time funding fee) | Veterans, active duty |

| USDA | 0% | 640 | Annual fee (lower than PMI) | Eligible rural areas, income limits |

Estimated Monthly Payment by Loan Type ($600,000 home)

| Loan Type | Down | P&I | MI | Tax + Ins | Total |

|---|---|---|---|---|---|

| Conventional 20% | $120,000 | $3,193 | $0 | $663 | $3,856 |

| Conventional 5% | $30,000 | $3,792 | $285 | $663 | $4,740 |

| FHA 3.5% | $21,000 | $3,855 | $265 | $663 | $4,783 |

| VA 0% | $0 | $3,992 | $0 | $663 | $4,655 |

| USDA 0% (eligible) | $0 | $3,992 | $175 | $663 | $4,830 |

USDA has income and geographic limits; a $600K home is above many USDA-eligible price points in NOVA. VA loan amounts above the conforming limit may require a small down payment in 2026.

VA loans deliver the best monthly value for those who qualify — no PMI, full 100% financing — even with the funding fee included in the rate. For non-veterans, conventional with 20% down minimizes long-term cost; FHA and conventional with 3%–5% down get you in the door faster.

Run the Numbers

What Will Your Monthly Payment Be?

Use our mortgage calculator to estimate your monthly payment for any home price in Virginia, Maryland, or DC.

What Income Do You Need to Afford a $600,000 House?

Lenders look at debt-to-income ratio (DTI) — the percentage of your gross monthly income that goes to housing and other debts. The traditional rule of thumb is a 28% front-end DTI (housing only) and a 43% back-end DTI (housing plus all debts). Modern conventional loans can stretch to 45%–50% in the right scenario, but a 36% back-end is the financially comfortable target.

Income Required for a $600,000 Home (by DTI threshold)

| Scenario | Total PITI | Income (28% DTI) | Income (36% DTI) | Income (43% Max DTI) |

|---|---|---|---|---|

| 20% Down Conventional | $3,856 | $165,000 | $128,500 | $107,600 |

| 5% Down Conventional | $4,740 | $203,150 | $158,000 | $132,300 |

| FHA 3.5% Down | $4,783 | $205,000 | $159,400 | $133,500 |

| VA 0% Down | $4,655 | $199,500 | $155,200 | $129,900 |

Income figures assume no other debts. Each $500 of monthly debt (auto, student loans, credit cards) raises the income threshold by roughly $14,000–$17,000.

In the DMV, a household income of $150,000–$185,000 is the practical sweet spot for a $600,000 home with comfortable margin. With significant existing debts (student loans, car payments), or HOA dues over $300/month, you'll need to be at the upper end of that range or above.

Closing Costs on a $600,000 Home in VA, MD, and DC

Closing costs are the fees and taxes you pay at settlement, separate from your down payment. On a $600,000 purchase in the DMV, expect closing costs to run 2.0%–3.5% of the purchase price. Here's a typical itemization for a Virginia closing.

| Closing Cost Item | Estimated Range | Notes |

|---|---|---|

| Lender Origination & Processing | $1,200–$2,500 | Negotiable; varies by lender |

| Appraisal | $650–$900 | Required by lender |

| Credit Report | $60–$120 | Pulled by lender |

| Title Insurance (Owner's + Lender's) | $2,200–$3,200 | Owner's policy is optional but strongly recommended |

| Settlement / Attorney Fees | $700–$1,400 | Title company or attorney |

| VA Recordation Tax (state portion) | $1,500 | $0.25 per $100 on deed |

| VA Local Recordation Tax | $500 | 1/3 of state tax (varies by county) |

| Deed of Trust Tax | $1,500 | $0.25 per $100 on loan amount |

| Survey (sometimes required) | $400–$700 | Common in VA |

| Home Inspection | $500–$700 | Optional, paid before closing |

| Prepaid Property Tax & Insurance Escrow | $3,500–$6,000 | Funds your escrow account |

| Total Estimated Closing Costs | $13,000–$22,000 | Approximately 2.0%–3.5% of price |

In Maryland, the recordation tax structure is different (each county has its own rate), and Maryland charges a state transfer tax that's often split between buyer and seller. In DC, recordation and transfer taxes are higher overall — typically 1.1% (or 1.45% above $400,000) of the purchase price each, though buyers often qualify for the DC Homestead deduction or first-time buyer recordation tax reduction.

Property Taxes by DMV County (on a $600,000 Home)

Where you buy directly affects your monthly payment. Below are real 2025–2026 effective rates applied to a $600,000 assessed value.

| Jurisdiction | Effective Rate | Annual Tax | Monthly Escrow |

|---|---|---|---|

| Loudoun County, VA | ~0.92% | $5,520 | $460 |

| Fairfax County, VA | ~1.10% | $6,600 | $550 |

| Prince William County, VA | ~1.04% | $6,240 | $520 |

| Arlington County, VA | ~1.01% | $6,060 | $505 |

| Alexandria City, VA | ~1.11% | $6,660 | $555 |

| Montgomery County, MD | ~1.00% | $6,000 | $500 |

| Frederick County, MD | ~1.06% | $6,360 | $530 |

| Prince George's County, MD | ~1.32% | $7,920 | $660 |

| Washington, DC | ~0.85% | $5,100 | $425 |

Rates rounded for illustration. Actual rates change annually and may include local additions. DC has the lowest effective rate but offsets it with higher recordation/transfer taxes at closing.

The difference between Loudoun (the lowest NOVA tax county) and Prince George's MD on a $600,000 home is roughly $200/month — or $72,000 over 30 years. Where you buy matters as much as the price you pay.

Ready to Start Your Search?

Browse $600,000 Homes in Northern Virginia

Once you know your budget, explore available homes across Loudoun, Fairfax, Prince William, Arlington, and Alexandria.

How Interest Rates Change Your Payment

Each percentage point change in your interest rate makes a meaningful difference in your monthly payment. Below shows P&I on a $480,000 loan (a $600,000 home with 20% down) at different rate scenarios.

| Interest Rate | Monthly P&I | Difference vs. 7% | 30-Year Interest |

|---|---|---|---|

| 5.0% | $2,577 | −$616/mo | $447,720 |

| 5.5% | $2,725 | −$468/mo | $501,000 |

| 6.0% | $2,878 | −$315/mo | $556,080 |

| 6.5% | $3,034 | −$159/mo | $612,240 |

| 7.0% | $3,193 | — | $669,480 |

| 7.5% | $3,356 | +$163/mo | $728,160 |

| 8.0% | $3,522 | +$329/mo | $787,920 |

Hypothetical scenarios for illustration only. Rates change daily — current rates are available through your lender.

A 1% rate change shifts your monthly payment by about $315 on a $480,000 loan and changes your total interest paid over 30 years by roughly $113,000. This is why rate locks, buy-down strategies, and timing matter — and why working with a lender who can show you several rate-and-fee combinations beats taking the first quote you see.

Total Cost Over 30 Years

Most buyers focus on the monthly payment and forget that, over 30 years, the loan's total cost includes hundreds of thousands of dollars in interest. Here's what a $600,000 home actually costs over the life of the loan.

| Cost Component | 5% Down (7% rate) | 20% Down (7% rate) |

|---|---|---|

| Down Payment | $30,000 | $120,000 |

| Total P&I (30 years) | $1,365,120 | $1,149,480 |

| Total Interest Paid | $795,120 | $669,480 |

| PMI (until 78% LTV) | ~$25,000 | $0 |

| Property Taxes (NOVA, est.) | ~$220,000 | ~$220,000 |

| Homeowners Insurance | ~$70,000 | ~$70,000 |

| Total Outlay (30 years) | ~$1,710,120 | ~$1,559,480 |

Tax and insurance figures assume modest annual increases. Actual figures will vary based on rate environment and tax assessments.

The 5%-down buyer pays roughly $150,000 more over 30 years than the 20%-down buyer — but kept $90,000 in their pocket up front and started building equity 2–4 years earlier. Whether that's worth it depends on what you do with the cash, how the home appreciates, and how long you stay.

7 Ways to Lower Your $600,000 Mortgage Payment

If the standard scenarios above stretch your comfort zone, there are several legitimate strategies to bring down your monthly payment without leaving the $600,000 price point.

- Buy down your rate (temporary or permanent). A 2-1 buydown lowers your rate by 2% in year one and 1% in year two. A permanent buydown costs 1 point (1% of loan) for roughly 0.25% rate reduction — saving $80–$100/month for the life of the loan on a $480K loan.

- Increase your down payment to 10% or 20%. Eliminates or reduces PMI; on a $600K home, going from 5% to 20% saves around $285/month in PMI plus reduces P&I by another $600/month.

- Consider a 7/1 or 10/1 ARM. ARMs typically offer lower introductory rates than 30-year fixed mortgages — useful if you plan to sell or refinance within 7–10 years. The trade-off is rate uncertainty after the fixed period.

- Pay off other debts before applying. Each $500/month in non-housing debt eliminated raises your borrowing capacity by about $80,000 — or lets you put more cash toward your down payment.

- Boost your credit score. Going from 680 to 760 typically saves 0.25%–0.50% on your rate, plus reduces PMI cost. Pay down credit card balances 30+ days before pre-approval.

- Shop multiple lenders. Rate, fee, and pricing variations of 0.25%–0.5% are common. Get Loan Estimates from at least 3 lenders within a 14-day window to keep your credit-pull impact minimal.

- Use down payment assistance. Virginia Housing offers a down payment grant up to 2.5% of the loan amount for first-time buyers; DC HPAP provides up to $202,000 in assistance for eligible buyers; Maryland MMP includes Smart Keys and Maryland HomeCredit. These can dramatically reduce your cash needed at closing.

Free · No Commitment

Get Pre-Approved for a $600,000 Mortgage

A 10-minute pre-approval gives you a real loan amount, exact monthly payment, and the leverage to win competitive offers in the DMV.

Ken Byrne NMLS #187129 · ALCOVA Mortgage LLC NMLS #40508

Selling Your Current Home to Buy a $600,000 House?

If you're a move-up buyer, the equity in your current home is likely your biggest source of down payment cash. Reducing what you pay in listing commission directly increases the proceeds you can roll into your next home — a 1.5% listing commission instead of the traditional 3% can add $9,000–$15,000+ in spendable equity on a typical DMV sale.

For Move-Up Buyers

Sell at 1.5% Listing Commission

Keep more of your equity to put toward your $600,000 purchase. Full-service listing for half the traditional commission.

Frequently Asked Questions

How much is a mortgage on a $600,000 house?

A mortgage on a $600,000 house in the DMV typically runs $3,900–$4,950 per month including principal, interest, property taxes, homeowners insurance, and mortgage insurance. With 20% down ($120,000), expect roughly $3,856/month total. With 5% down on a conventional loan, expect about $4,740/month.

What income do I need to afford a $600,000 house in Northern Virginia?

Most buyers need a household income of $150,000–$185,000 to comfortably afford a $600,000 home in Northern Virginia, depending on their down payment and other monthly debts. Lenders may technically approve you up to a 50% DTI, but a 36% back-end DTI keeps your finances healthier long-term.

What credit score do I need for a $600,000 mortgage in Virginia?

580 for FHA, 620 for conventional and VA, 640 for USDA. Higher scores qualify for lower rates and lower PMI. Borrowers with 740+ generally see the best pricing on conventional loans, and at $600,000 the rate difference between 680 and 760 can be worth $200+ per month.

How much down payment do I need for a $600,000 house?

As little as 0% with a VA or USDA loan, 3% with a conventional first-time buyer program ($18,000), 3.5% with FHA ($21,000), or 5% with standard conventional ($30,000). For 20% down to avoid PMI, you'd need $120,000 cash. Down payment assistance programs in VA, MD, and DC can reduce these amounts significantly.

What are the closing costs on a $600,000 house in Virginia?

Expect $13,000–$22,000 in total closing costs for a $600,000 home in Virginia — roughly 2.0%–3.5% of the purchase price. This includes lender fees, title insurance, recordation taxes (Virginia charges $0.25 per $100 of the deed and the loan), settlement fees, prepaid escrows, and the appraisal. Maryland and DC have different recordation/transfer tax structures that often run higher.

Can I buy a $600,000 house with a VA loan?

Yes — VA loans have no maximum loan limit for buyers with full entitlement, meaning you can finance the entire $600,000 with $0 down. The VA funding fee (1.25%–3.3% depending on use and down payment) can be rolled into the loan. VA loans are exceptionally well-suited to NOVA's military buyer population from Fort Belvoir, Quantico, and Pentagon assignments.

Is a $600,000 house cheaper in Virginia, Maryland, or DC?

Monthly carrying costs are typically lowest in DC (lowest property tax rate at ~0.85%) and highest in Prince George's County, MD (~1.32%). However, DC has higher recordation/transfer taxes at closing. Loudoun and Arlington fall in the middle for ongoing carry. The right answer depends on whether you optimize for upfront cost or 30-year cost.

What's the conforming loan limit for a $600,000 mortgage in the DC metro?

For 2026, the conforming loan limit in the DC metro high-cost area is $1,249,125 for a single-family home. A $600,000 loan is comfortably within conforming limits, so you'll get standard conventional pricing — no jumbo loan upcharge required.

How do PMI and FHA MIP differ on a $600,000 house?

PMI on a conventional loan automatically drops at 78% loan-to-value (LTV) and can be requested for removal at 80% LTV. FHA MIP, in contrast, stays for the life of the loan if your down payment is below 10% — so most FHA buyers eventually refinance to conventional once they hit 20% equity. On a $600,000 home, this difference can be $250–$300/month for the long term.

Can I get down payment assistance on a $600,000 house?

Yes — many DMV programs work on $600,000 purchases. The Virginia Housing DPA Grant (up to 2.5% of the loan) requires meeting income and price limits but applies in many NOVA counties. DC HPAP can provide up to $202,000 in assistance for eligible DC buyers. Maryland MMP offers Smart Keys, HomeCredit, and Partner Match programs. Income and purchase price limits vary by program and county — review eligibility with your lender early.

Should I buy a $600,000 house with 5% down or wait for 20%?

Depends on your timeline and the market. Putting 20% down saves PMI and reduces your payment by hundreds per month — but the time it takes to save another $90,000 in the DMV is often two to four years, during which home prices and rents typically rise. For many buyers, buying at 5% down sooner and paying down to 20% equity over time is the better long-term math.

How do I find a good mortgage lender for a $600,000 home in Northern Virginia?

Look for a licensed loan officer (verifiable at nmlsconsumeraccess.org), strong DMV market knowledge, responsive communication, a full slate of loan programs (Conventional, FHA, VA, USDA, jumbo, Virginia Housing), and transparent fees disclosed in a Loan Estimate. Ken Byrne (NMLS #187129) at ALCOVA Mortgage LLC (NMLS #40508) operates JB Financing and serves buyers across Virginia, Maryland, DC, and West Virginia.

Glossary of Mortgage Terms

PITI: Principal, Interest, Taxes, Insurance — the four core components of your monthly mortgage payment.

PMI (Private Mortgage Insurance): Required on conventional loans with less than 20% down. Drops automatically at 78% LTV.

MIP (Mortgage Insurance Premium): The FHA equivalent of PMI. Stays for the life of the loan if down payment is below 10%.

DTI (Debt-to-Income Ratio): The percentage of gross monthly income that goes to debts. Front-end = housing only; back-end = housing plus all debts.

LTV (Loan-to-Value): The loan amount divided by the home's value. 95% LTV = 5% down. PMI typically drops at 78% LTV.

Conforming Loan: A loan that meets the size and underwriting standards of Fannie Mae or Freddie Mac. The 2026 DC metro conforming limit is $1,249,125.

Recordation Tax: A Virginia state and local tax paid at closing to record the deed and deed of trust. Typically about 0.5% of the purchase price combined.

Escrow: An account your lender uses to hold and pay your property taxes and homeowners insurance on your behalf throughout the year.

Bottom Line

A $600,000 house in the DMV is genuinely affordable for buyers in the $150,000–$185,000 income range — and even more accessible for VA-eligible buyers and those who use down payment assistance. The path to your number isn't guesswork; it's getting a clear pre-approval, running real scenarios with a lender who knows the local market, and building a budget that includes every line item — not just principal and interest.

Ken Byrne and the team at JB Financing / ALCOVA Mortgage have helped hundreds of DMV buyers navigate this exact decision. The first step is free, takes 10 minutes, and gives you the certainty to make confident offers.

Ready to Move Forward?

Get Your Personalized Mortgage Quote

No obligation. Real numbers based on your actual financial profile — for any home price in VA, MD, or DC.

Ken Byrne NMLS #187129 · ALCOVA Mortgage LLC NMLS #40508

Disclaimer: This article is for informational purposes only and does not constitute financial or legal advice. Mortgage programs, rates, and eligibility requirements are subject to change. Contact a licensed mortgage professional for guidance specific to your situation. Ken Byrne, NMLS #187129 · ALCOVA Mortgage LLC, NMLS #40508 · Licensed in VA, MD, DC, WV.

Categories

Recent Posts

GET MORE INFORMATION

Broker Associate